Musings on business models for Alpha School

Alpha School has exploded into the public dialogue in recent weeks. I was first exposed to it when Colossus did a long-form piece on its dean of parents, principal and lead backer, Joe Liemandt. An Invest Like the Best episode with Liemandt followed, along with a number of other interviews.

Education in this country obviously has a massive opportunity to improve. One teacher lecturing to a class of 19 students on a fixed curriculum at a fixed pace just can't be the best way for each individual student to learn. And, because it has been run by the government, it hasn't been a place that has seen any innovation.

AI has reached a point of critical advancement that has opened the aperture of practical applications. K-12 education is one of them. The premise for Alpha School: AI-driven learning software, provided to students on a tablet, enables students to learn 2.6x faster (measured on MAP score improvement) with 2 hours of dedicated learning time per day. The rest of the day is then allocated to learning life skills in ways that are fun for kids, in part because if they have completed the 2 hours of course work, they have agency - the reward - to influence the balance of their day.

Since I'm a business fanatic, the lens through which I'm most interested in discussing Alpha is the business model. I have much to learn, but the purpose of this is to jot some musings, provoke discussion and surface some questions.

I was intrigued that Liemandt, on a recent podcast, talked about the Alpha business model - the physical school part of the business - looking like Chipotle.

"...can model this right after Chipotle. Business model-wise, same margins, a lot of the same expertise, I need retail because I need 500 of these outlets, high standards, I’m gonna build this as big as Chipotle. There’s gonna be one of these everywhere.”

In other words, a large part of Alpha is really a 4-wall business model. In my ~11 years of investment banking, a much of my time has been spent on the 4-wall model, which added to my intrigue.

The barometer of success of any 4-wall business model is the cash-on-cash return of each unit. In this case, each new school. One school costs $X to build, and each year it produces $Y of cash flow. $Y divided $X needs to be compelling enough for unit growth to continue. In my experience, a good return (pre-tax cash flow) here is 30%, and great is over 50%. Chipotle is in great territory, having sustained something like 60% cash-on-cash returns. Starbucks (until maybe recently) has also been in great territory. The return on each unit here is not the overall business's return on capital, because there is G&A and overhead, etc. But the yardstick remains.

Interestingly for Alpha, there is another component of its business model that almost all other 4-wall businesses don't have: the proprietary engine of the curriculum, the AI-driven software they have adeptly named Timeback (they are giving kids their time back!). Gun to my head, I would say this is where the value at Alpha is going to be manifested 10 years from now; not because the whether the software itself will be difficult to replicate, but because of the value of the ecosystem it might create and the insights about how kids learn it could reveal.

What could the 4-wall economics look like?

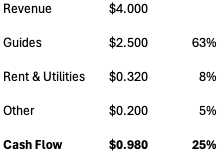

I'm estimating with limited information, but for revenue at each school, let's use 100 students paying $40k per year per student. This means each school would have $4m revenue.

There is apparently a 5:1 student-to-guide ratio at the Austin schools (I believe this is the most "mature" Alpha market). This would mean 20 Guides at the 100-student Alpha School. If each guide is paid on average $125k, that means each school would pay its Guides $2.5m per year. (The students per school is illustrative; the 5:1 ratio is what drives the margin structure).

Assuming rent and utilities of 8% (Chipotle is ~5%, Mathnasium is ~15% with sub-$1m sales and smaller sq. ft. footprint), and other expenses (e.g., supplies) of 5% of revenue, cash flow margin is 25%.

If the student-to-Guide ratio were to increase, the cash flow margin would scale significantly as the semi-fixed cost of Guides would stay the same or increase at a slower rate, and you've have leverage on the fixed facilities costs (rent & utilities).

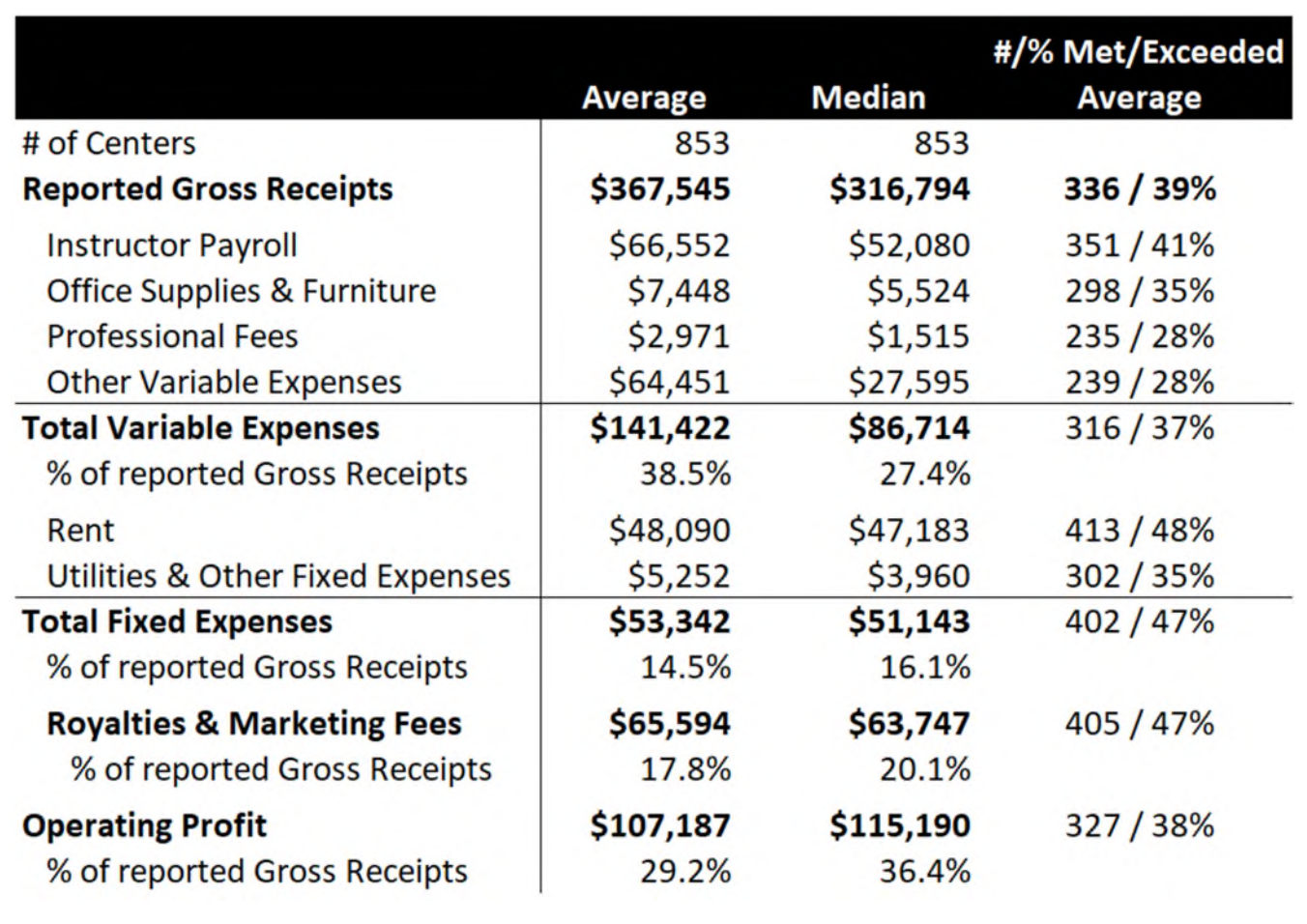

I mentioned Mathnasium, which is a franchised concept that focuses on math tutoring only. If I were looking to value Alpha's 4-wall business only, I would be looking at Mathnasium as one of several comparable businesses. The average P&L from Mathnasium's FDD is below, and it shows a 29% cash flow margin. While restaurants are a different business model (largest costs are usually food & beverage at 30%, labor at 30-35%, rent at 5-10%, and other at 10-20% which is a catch-all and more variable range), Chipotle has been in the high 20s for restaurant-level EBITDA (i.e., proxy for cash flow) margin. High-20s margin for restaurants is very good.

I'm not sure how much an Alpha School costs to build, but I would think that within the four walls, it's tables and cubicles and furniture driving most of the cost. For simplicity, I will assume that the iPad or computer that students use is covered in the cost of the tuition or paid for outside of Alpha. Mathnasium build costs are about $107 per sq. ft. If an Alpha has 100 students and 20 Guides, let's say there are 20 class spaces at 1,000 sq. ft. each, so 20k sq. ft. in total. If it costs $100 PSF to build, that means build cost is $2.0m.

So the cash-on-cash return here would be $980k / $2.0m or 49%. There are a handful of assumptions that went into this (the ones I walked through above), so I am a little cautious here, but a 50% return that's sustainable points to a very nice 4-wall business that would be attractive to investors.

The revenue or tuition per student is going to be the key variable to watch (maybe obvious). There seems to be a range of $40k to $75k today depending on the market (coastal is higher, also obvious to expect). But what happens over the years if government were to subsidize tuition? Or Alpha adopts a strategy to lower the cost to encourage more enrollment (as they might have the margin to do so, strictly on a 4-wall business basis; they may be piloting this already with $10k tuition cost at Brownsville, TX)? As other similar businesses, and Alpha itself, proliferate, increasingly supply of options should push price down.

The largest cost at the 4-wall side of the business is the cost of the Guides. As students get older, I would think the student-to-Guide ratio can increase. Every student added to that ratio would be pure margin. The Guides are not trained as teachers, and do not have to be educated as teachers, so the bar to admit Guides could presumably be lower, and therefore a greater pool of willing people to be Guides, and therefore a lower required salary to pay. I would want to understand how much of an impact the quality of the Guides has on students' futures...my current guess is high-ceiling, high-floor...an excellent Guide might mean the world to a student's future, but an average one isn't going to harm the student to high degree?

What else could you do with the 4-wall business part of the model?

Real estate

I suspect that finding real estate, or specific sites, is a limiter of the growth of Alpha. Finding a small number of real estate partners could be interesting for securing growth. This is how Topgolf scaled initially – they worked with EPR Properties who was the primary real estate partner. The similarity between Alpha and Topgolf at this stage of Alpha's life cycle is they have relatively new business models that real estate investors are not used to underwriting. So, if one real estate financing partner can get behind Alpha and understand its 4-wall economics intimately, this could help accelerate Alpha's growth by removing or mitigating a key growth limiter.

Howard Hughes is a real estate company that basically focuses on upper middle class master planned communities (residential and mixed-use). It would make sense for Alpha School to be near these, as the wealthier buyers of the lots in these MPCs probably fit the current profile of Alpha parents. Over time, the average Alpha parent is going to include more middle class, but for the current growth stage, something like this could make sense. For Howard Hughes, it enhances the value of the MPCs and helps monetize land. For Alpha, it secures growth and keeps them out of real estate business. Generally, I have the view that 4-wall businesses should be leasing, not owning, real estate. They are totally different asset classes with different expected returns and therefore should have different capital backing each asset.

Interestingly, Bill Ackman, whose investment business now controls Howard Hughes and is building it into a holding company, has been publicly praising Alpha School. I would not be surprised if some discussion like this around HHH and Alpha School real estate has already occurred.

Using new MPCs to find new sites for Alpha scales Alpha in 2+ years from now, but not today. I suspect there are simple tactics such as top metropolitan cities and looking for a combination of brands like Whole Foods, Trader Joe's, lululemon, Tesla, etc., where if there's a retail presence of all three in X mile radius, this is an affluent market that could support an Alpha earlier in Alpha's growth stage. Maybe the top 50 or 75 cities by population could support at least one? I grew up in Madison, WI, which is about at rank 75, and I'm sure it could support at least one Alpha (one of my best friends attended a private middle school almost 20 years ago, and Madison has grown and become more affluent since then). Maybe there's a common characteristic(s) among iconoclastic-thinking parents that could be used to gauge market viability?

With mid-teens number of markets/cities now, maybe there's enough there to develop adjacent locations within each market. This market clustering strategy is one that restaurant companies have been deploying, but it's a little different here because a student/family doesn't use multiple school locations in each market. However, word of mouth and building the anecdotal recommendation engine might be the best marketing there is for Alpha.

When Timeback is released to more homeschoolers or micro schools, maybe this will be a way to see geographic clusters of activity that will point to new opportunities for a physical Alpha.

Franchise

The 4-wall model could be franchised rather than owned by Alpha. This would take the capital burden off of Alpha, and could probably scale the business faster. However, with cash-on-cash returns of 50%, that is a lot of economics to give away.

The actual execution of the schools - Guiding the students, interacting with parents - might be straightforward, which lends itself to franchising. If Alpha feels there is limited secret sauce here, that would be an argument for franchising.

Value of the proprietary software, Timeback

As mentioned, this is where I would suspect the most value to manifest over the years as Alpha grows. The reason is I think it could get more useful and therefore more valuable the more kids use it.

Obviously, Timeback has a cost. And probably a very big one given the engineering and development talent that goes into most successful software, plus the ongoing cost to defend against obsolescence (caveat: this is probably a simplification, I have not studied software businesses in detail, but the point is, software can have a high upfront cost and requires ongoing costs to maintain the value of the asset). This cost cannot be ignored in the context of the 4-wall business above, but maybe there are ways to separate the businesses.

For example, Timeback is its own business but charges a technology fee to each Alpha School, or each school entity using Timeback. It's effectively the same as McDonald's charging its royalty to each franchisee. Or, there could be a separate subscription fee to the Timeback business that gets added to the tuition cost. Over time, this fee could decline.

Network effect

With a network effect, the more hours that are logged on Timeback by students actually using it, the better the product becomes. This is like the neural network at Tesla. More miles driven = more learnings = improved Tesla software. The improvements are rolled out to users in real time.

Is Timeback creating a graph?

Maybe an even more exciting implication of the Timeback software is that it could create a graph with several valuable uses.

By graph I mean nodes and edges. Nodes are an entity/data point/fundamental unit, edges are the connections between nodes. An example is a social network, where each person is a node and connections/communications/messages between each person are edges. The Tesla network is a graph - each car is a node, and information about how each car has driven is connected to a central data repository/HQ.

One potential result of Timeback as a graph, nodes to a central node: it learns and draws new insights about how kids learn. In other words, it advances learning science, because it is collecting the world's largest network of data on real kids learning real things. This kind of data has never been captured at mass scale. What's the goal of learning faster anyway? Yes, there are basic things to learn like math and grammar and social sciences, etc. But this is curriculum based. Could we use Timeback to understand how each student learns best, then implement ways to help them learn better based on this? Learning how to learn - in the context of each student him/herself - might be the greatest life skill of all.

Another potential result of Timeback as a graph, nodes to other nodes: it creates an interest graph among other students. Imagine if you were a student using Timeback, and you could meet other students across the country who have similar skills as you do, and similar interests, and think in the same way...you have a tool to "find your people." Since I'm a business nerd, this makes me think of the initial meeting between Warren Buffett and Charlie Munger, who became inseparable business partners and friends over decades. They happened to meet at a dinner because a mutual connection thought they'd hit it off...the rest is history, over a trillion dollars of equity value created. What if we had a tool like this for everyone to tap into? To find their people at say age 14? That would be life-changing.

Speed of scale?

There is potentially a lot of value if you have a platform that successfully achieves untouchable scale first, such as Netflix and Spotify. Also known as first-mover advantage. Especially if Timeback gets more valuable as more students are on the platform, you would want to scale that faster than your nearest competitor.

That said, the benefits of Netflix's and Spotify's scale mean that they can pay for content at a price that is much cheaper per subscriber than any of their platform competitors. This effectively extends their lead and moat so long as they have the subscriber scale. For Timeback, it does not have the need to continually purchase content, so I wouldn't think the benefits of scale are as critical to Timeback.

However, if Timeback wanted to subsidize tuition for any reason, or for any specific markets or cases, etc., then having this scale as inputs might then have some additional benefit. But does the incremental student provide as many units of value to Timeback as the incremental unit of content does to Netflix? I don't know enough to answer that question.

Value to price

I believe Netflix and Spotify both think about their value-to-price ratios. It is less of a data analysis exercise as it is to a holistic one. If I paid $15 per month 10 years ago, and I'm paying $18 per month now, did I get more than $3/month of value in those 10 years? The answer is an astounding yes, and speaks to the mouth watering pricing power those platforms have to this day (I would argue it's growing and will continue to grow because they can buy content for the cheapest price per subscriber than anyone else in the world).

For Timeback, this could be a compelling metric to guide the business. If they build a lead, if they build a graph or more than one graph, they will have created something that probably provides much more value than each student pays for it.

Various questions

What's going to push and pull on tuition price per student? Supply/demand factors, government subsidies (state and federal)?

What would happen if MAP testing goes away? What would be the learning yardstick? Is there an absolute target we should be thinking about? In the long run, if most students were to learn the basic things faster and therefore earlier, what else would we add to the curriculum? Where would that stop? Does there need to be some sort of feedback guidance on what it means to be an effective human in this world?

What will be the limiters of growth? Is there any reason to limit growth in exchange for building a more sustainable, high-integrity business? Costco was maniacally focused on keeping prices low by setting a maximum margin, and its limiter on growth is general manager talent (to this day), but they like it this way.

How critical are Guides to the overall quality of the product?

How will regulators get in the way? How do you bring capitalism to education (i.e., Alpha) in a win-win way? How do you prevent it from becoming a quasi-subsidized government-run business like Healthcare?

How is Timeback best monetized? Does speed of scale matter?

Other than Timeback, what can Alpha build to deepen its moat? Why go to Alpha or an Alpha brand over other schools? Is there something to do here with the life skills part of the day? What about understanding emotions? What about self-love? Can you combat childhood lowercase-T traumas in real time?

What are the implications of the graph(s) that Timeback is creating?