Part 1: What’s a Goosehead?

Introduction to Goosehead, a personal lines independent insurance agency

You’re at your kitchen counter, sitting beside your fiancee with your laptop in front of both of you, because you’re starting to look for a flight to Europe. The flight is for your honeymoon, so it is a once-in-a-lifetime trip. Neither of you has ever been to Europe, and you don’t know much if anything about booking travel to Europe. But you have the dates locked down, so you’re ready to look for flights.

Your Aunt Bertie is a frequent traveler to Europe, and she has flown only one airline for years. She books direct, no matter the route or fare class or flight times. “The price is the price, just book it. I’ve never had a problem with them in 20 years,” she says. “No need to price-shop, and you don’t need to use a travel agent. I’ll tell you what to do.”

Now, listening to Aunt Bertie’s advice here would be absurd. You’re buying probably one of the more expensive flights you’ve ever bought (particularly if you’ve never been overseas), there are many flight routes and destinations for flying to Europe, the fare class really matters for your flight experience and prices can range widely. Looking at all of the available flight options and prices is both easy to do and obviously the better way to buy this flight. And, we know there are sometimes discounts for booking flights, hotels and rental cars all together, which can take some finesse to optimize. We may love Aunt Bertie, but we aren’t going to just let her decades-long complacency limit the possibilities of our honeymoon.

You may even want a travel agent to help you elevate your experience and avoid common pitfalls, because they book this kind of trip every week as they do it for a living, and you simply have no clue when it comes to European travel. Better yet, an agent might have intimate local knowledge of the area of Europe you’re looking to visit. They also have an intuitive sense of getting the most bang for your buck depending on the experience you want to have. With a transoceanic journey representing a trip you’ll remember for the rest of your life, you know you’re making a large investment, and you want it to be worth it, so it’s easy to appreciate the value in working with a travel agent.

This experience of booking travel (here, to a faraway place you know nothing about) is not too dissimilar from buying homeowners insurance:

- especially for first-time homebuyers, it’s a highly considered, expensive and emotional purchase

- it’s your first time buying the product this way, and you don’t have a lot of knowledge about the product that has many details and micro-decisions to consider

- you want to see all the choices and options

- you don’t want to overpay

- you’re willing to listen to expert advice

- you want a good experience and proper coverage if something bad happens

Unfortunately, homeowners insurance is still commonly bought the way Aunt Bertie buys her flights and books her travel to Europe. There is a better way.

What this is about and what we’re discussing in Part 1

A few months ago, curiosity led me to the insurance agency business. It started on the commercial lines side, because with my interest in learning about a variety of businesses, a business whose customers are businesses themselves is always interesting. It also doesn’t take long to figure that the insurance agency business is a nice business and will be for a long time:

- distribution business that is driven by transaction volume often for a required, non-discretionary product

- much better than the insurance underwriter / carrier business, which involves a lot of capital, the very difficult task of pricing risk at a profit and therefore suffers from thin margins

- highly recurring revenue where policy renewal rates even for the worst salespeople are over 80%

- does not require significant capital to start or to grow

- high-margin business, usually 20-30% operating margin

- increasingly dynamic world with new and increasingly numerous risks

- very high likelihood that businesses and people will be buying insurance 100 years from now; protecting risk is fundamental to the human psyche and personal finance hygiene

Cold outreach and conversations with a number of independent insurance agency owners led me to a conversation with a former Goosehead employee, who introduced me to a current employee. Since then I reached out to current Goosehead franchise agency owners, about 15 of them, and I’ve been learning more about the business.

Goosehead is an independent agency in the P&C personal lines industry with a corporate and franchised agency model.

This is Part 1 and will focus on the consumer insurance buying experience (primarily home insurance), how that experience ought to be and how Goosehead is set up to provide that experience for the consumer; it also discusses how the Goosehead model is effective for the insurance agent.

Part 2 will discuss relevant industry trends, which provide validation for the independent agency model.

Part 3 will share the insights from my conversations with the 15+ Goosehead agency owners.

Part 4 will analyze Goosehead as a whole, from an investor’s perspective. Goosehead is a publicly traded company.

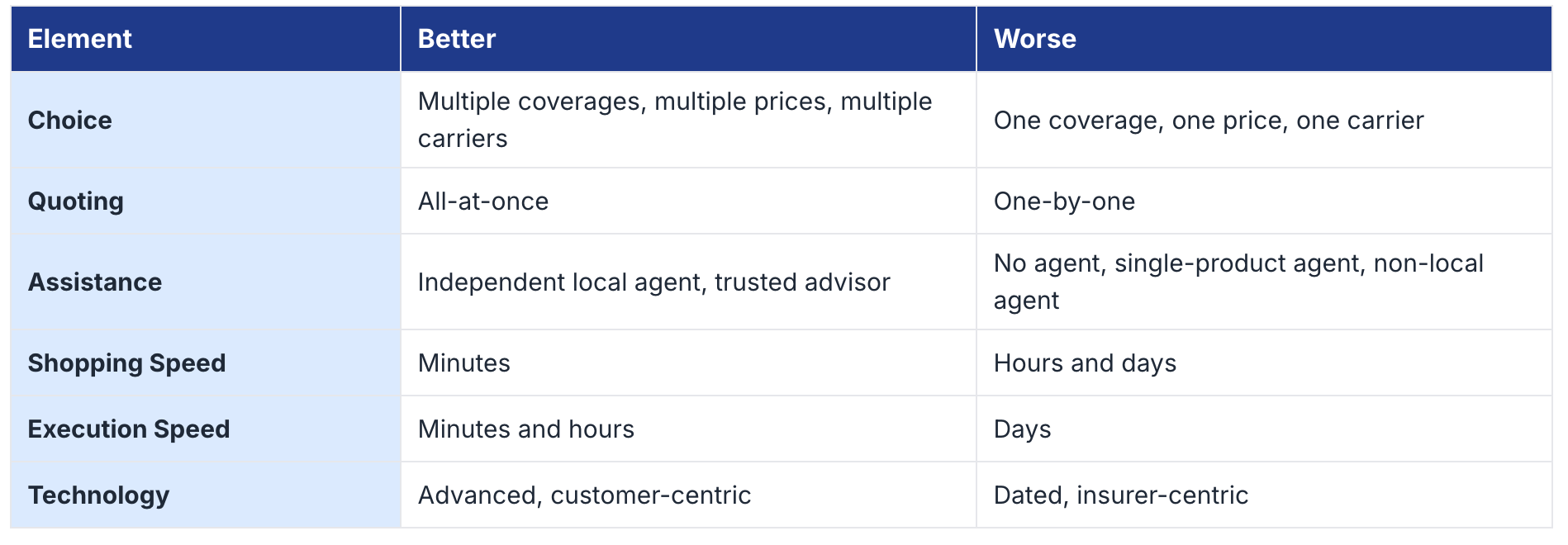

How home insurance ought to be bought

If you’re buying a home with mortgage (most Americans), the bank requires the homeowner to have insurance. This is because the bank effectively owns the home and it needs to protect the value of the asset underlying its loan. Even if you’re flush with cash and buy a home outright, you’d be prudent to have insurance — homes are expensive things to repair and replace, and they are usually one of the largest if not the largest “asset” in a homeowner’s net worth. So, home insurance is one of the more non-negotiable, must-have products anyone can buy.

While the insurance policy itself — the promise of the insurer to pay for damages caused by certain events — is a commodity, each policy is by default customized for each home. There are many variables that an underwriter needs to understand to assess the risk of a loss event on any given home: geography and climate conditions, loss history, age of home and particular components such as the roof and HVAC system, construction type, size, foundation type, homeowner profile, additional risks such as dogs and pools, etc. In other words, the inputs that are needed to provide a policy are numerous and they are not necessarily simple. For a complete and accurate home insurance quote, it is not uncommon to provide 300-400 units of data.

There is also the context and situation in which the product is bought. For a first-time homebuyer, the situation is that they’re probably making the largest financial decision of their life (emotional!); buying a home comes with a slew of decisions to be made; and there is a process timeline to follow — offer, offer negotiation and acceptance, appraisal, loan approval and closing. So it’s an emotional, multi-part process with a lot of money at stake, often done on a tight timeline. Given the situation, what’s important for an insurance policy is that it a) has coverage that is satisfactory for the lender and the buyer, b) has a price (called “premium”) that is satisfactory for the lender and the buyer, and c) can be processed and bound quickly within the home buying timeline. Price is particularly notable because the premium will be considered by the lender in the affordability equation for the buyer — if the buyer is approved for a home cost of 50% of his monthly gross income, the insurance premium is part of that 50%. If the buyer is already stretching on his home purchase price, it would be a shame for the insurance premium to tip it over the edge to a non-approval. Speed also cannot be understated, as we will discuss later.

With all of this in mind, we can lay out how a home insurance policy ought to be bought:

Goosehead was created to make a better buying experience for the consumer

Goosehead was founded in 2003 by a wife and husband team, Robyn and Mark Jones. Robyn was raising six kids and got into flipping homes while her husband Mark was a frequently traveling management consultant for Bain. In flipping homes was how Robyn discovered the home insurance industry didn’t offer a good buying experience.

From Goosehead’s first earnings call as a public company:

My wife, Robyn, and I founded the company in 2003 starting with a blank sheet of paper. After multiple poor experiences with many insurance agencies, we knew there had to be a better way to deliver personalized insurance products to consumers and provide a full service experience that we and many others really need. From day 1, we put the client at the center of our universe and focused relentlessly on meeting their needs and giving them an effortless experience.

What Robyn and Mark created was an insurance buying model that is a win-win-win for buyers, insurance agents and insurance carriers. We’ll look at the first two in more detail.

What was on that blank sheet of paper? Looking at the Goosehead model as a buyer

Let’s first look at how Goosehead has optimized for the traits above from the perspective of the consumer, or the person buying insurance. I don’t actually know what was on that piece of paper, but I suspect it included the points below. A helpful framing for this is asking the question, “How can I get the insurance coverage I need, at the best price available, in the easiest way possible?”

Independence

Goosehead is an independent agency, meaning Goosehead provides insurance from more than one carrier or insurer, compared to a State Farm agent, for example, who can offer only a State Farm policy. When consumer buys insurance from an independent agent, he’s going to see multiple options and prices. When carriers pull back and are more reluctant to write policies depending on the environment, having this choice is valuable. With a single option from one carrier, the buyer could be overpaying or getting inadequate coverage for her risk tolerance.

Choice and Local Availability

Goosehead has access to over 200 carriers and reaches 98% of the U.S. population. For the insurance buyer, this means it’s likely that the choice Goosehead offers is going to be available to him. Given the national scale and volume of business it does with its carrier partners, it also means that this level of choice may be accessible only through scaled independent agency platforms like Goosehead and not any independent local agent. To be able to offer enough choices, an agency needs enough carrier partners, and to get enough carrier partners, an agency needs scale.

Human Touch

Buyers of a new insurance policy have access to an agent who knows the market and who is knowledgeable in home insurance. They also probably know recent local market dynamics — which carriers are writing good policies lately, which carriers have been raising prices, which carriers have been pulling back, which carriers are more likely to be a fit for your situation. Buying directly online does not provide these benefits.

Goosehead’s producer recruiting model is deliberate — it targets younger, hungrier people. These people are typically in their early- to mid-20s, recent college graduates or a couple years removed. They tend to have high energy and high motivation. The founders noticed that before they started the business, insurance agents were mostly older, not hungry or motivated, did not operate with speed (which is important!) and weren’t necessarily delivering consistent intellectual firepower. The average age of a personal lines insurance agent industry wide is in the 50s, with two-thirds over 40. Mark also ran recruiting at Bain, so he saw an opportunity where it made sense to deploy that talent acquisition playbook (Bain hires many recent graduates for entry-level consulting roles which are an important part of a consulting engagement team).

Technology

If technology can enhance the buying experience and the attributes above, then it should be integrated into the buying experience. This is even more true today than it was in 2003. For the buyer, an important benefit of the technology is speed. Speed helps with looking at multiple quotes at the same time and generally with the entire underwriting process. This is valuable when a home closing gets down to the wire, when holdups from insurance are unwelcome. After the initial purchase, the tech platform makes it easier for policyholders to make changes or add coverage. And when it comes time to renew the policy every year, Goosehead’s Digital Agent is a proprietary quoting platform, informed by hundreds of thousands of transactions from 20+ years of data, that makes the renewal process easier.

Looking at the Goosehead model as an agent

Say you want to become a personal lines insurance agent. What are your options?

- you could join an existing independent agency. But this path is as an employee, not an owner, and therefore dramatically less upside.

- you could join a captive agency like State Farm. It comes with all of the drawbacks which we have or will discuss in this Part 1. It also comes with the illusion of ownership of your book of business but is not ultimately economic ownership when you leave the system.

- you could start your own independent agency from nothing. Everything is directed on your own. You have to select and pay for your tech stack. Get all of the licensing done on your own. Try to get carrier appointments. Go out to market to get your first business. Be on your own with no shared best practices or learnings from being in the business. Be fully responsible for servicing all of your policies.

- you could join a cluster or network organization (like SIAA). This is better than starting your own agency, as it solves for the carrier appointments. And you get to keep the vast majority of your commissions. But you’re left with all of the other startup costs and challenges that go with starting from zero.

- you could join Goosehead as a corporate agent or a franchise agency owner. There are similar models to Goosehead like Brightway and Renegade, but they are smaller. You get a lot of carrier appointments, easy-to-use technology and a go-to-market playbook that works.

How should you choose? What are the big things that matter most?

Independence so you can provide policies from multiple carriers

You want to be able to offer policies from multiple carriers so your customers have choice in coverage and price. If your customer doesn’t have choices, you’re less likely to sell a policy.

You also want an adequate number of carrier appointments. As an agent, you can’t just call up any carrier like Progressive and expect to immediately sell policies on their behalf, especially if you have limited or no industry experience. Progressive wants to know they’re getting volume and quality insureds, and they don’t want to deal with tens of thousands of individual producers. Scale, by bundling many producers into one platform, solves this. So if you’re an agent, you want to be attached to a scaled distributor for several carriers.

High commission rates

As an independent insurance agent, your compensation is sales commissions, which are paid as a percentage of each policy’s premium. For personal lines P&C, this is usually 10-15%, with new business policies in the higher end of that range and renewals at the lower end. The more active policies in your book (policies in force), the more you’re getting paid. This means that you need to sell new policies and keep as many policies as possible on your book as they come up for renewal.

Obviously, you want the highest commission rates the industry has to offer. You don’t want to be disadvantaged by virtue of your employer or network. You would think that in a free market the commission rates available would be all about the same, but that is not in fact the case.

If you are an agent at a captive agency like State Farm, your commission rate is probably lower. You are also at the mercy of being connected to underwriting profitability, which is cyclical based on insurance rate swings. This means that if State Farm experiences a wave of losses from a weather catastrophe event, they will be looking for ways to reduce expenses to help stem underwriting loss. A Tegus interview with a former Goosehead employee mentioned that in 2015-2018, captives cut agent commissions by 40%. If you’re an agent, this lack of control is not attractive relative to alternatives.

Reliable and efficient way to find new business

Having a repeatable, relationship-driven playbook to find new customers at a low cost is ideal compared to spray-and-pray and paying for leads. The former takes less total effort over the long run, and allows you to monetize your expertise and reputation. The latter takes constant energy and dollars. The result is bind rates (the rate you actually sell a policy you’ve quoted) of 40-50%+ at an independent agency versus 10-20% at a captive.

Low-effort retention

Once you’ve sold a policy to a customer, you need to maintain and service the policy. This includes things like adding coverages, adding drivers on an auto policy, and proactively scanning rates and coverages ahead of renewal time. Personal lines policies are straightforward compared to commercial and other lines, so the servicing of these policies also tends to be straightforward on a relative basis. Servicing policies in a way that requires as little time and energy as possible to keep the policies on your book is ideal, which enables greater focus on adding more policies to your book.

Technology

Technology can enhance the speed of an agent’s entire operation — from figuring out where to find new business, to quoting and to servicing. Having this technology as a service, so you do not have to build it or maintain it, and at a low cost, is ideal.

Equity ownership

A book of insurance policies is a valuable long-term asset because of the nature of renewals. If you stopped selling new policies tomorrow, and your premium dollars retention is something like 85% per year (which is low for premium retention), it would take 14 years before your book dipped below 10% of the revenue that you had when you stopped selling new policies. So, having ownership in this book, instead of just annual commission dollars, is a world of difference. It’s why established insurance agents say things like “the amount you can make from selling insurance is one of the best kept secrets.”

What makes Goosehead’s model more valuable to agents than other models?

The value of Goosehead’s model comes from the combination of a few factors:

- Separation of sales and service

- New business generation by establishing relationships with home sale Referral Partners

- Proprietary technology to enable and enhance 1 and 2

Separation of sales and service

Goosehead made a pioneering move when it designed a personal lines insurance agency to separate sales and service (this was probably one of the big ideas on Robyn and Mark’s initial sheet of paper). Separating sales and service makes sense for two main reasons.

The first is that the person who is best at selling new policies is likely different than the person who is best at servicing policies. They are people with different talents and skill sets. It is the principle of comparative advantage. Let the hunters hunt and the farmers farm. People good at sales have high energy and motivation, handle rejection well, like talking to people and move with speed. People good at service might be more reserved, have high attention to detail and like following repeatable procedures with an objective of accuracy. Of course, you can find the person who would excel at both of these, but most of the time, people are going to be a better fit for one over the other.

The second reason is that it enables the producer (the agent who sells) to focus solely on sales. New business sales is the most valuable activity for any insurance book because the nature of a home insurance or auto insurance policy is one of low-resistance renewal. Once a policy is placed at a carrier, there is about an 85-90% renewal rate every year (all else equal, the coverage and price doesn’t change dramatically). So to increase the value of an insurance book, the highest priority is selling new policies. And by removing time and energy that would otherwise be needed to service policies, producers can focus solely on what matters most.

A typical non-Goosehead insurance agent with a somewhat mature book might devote 30-40% of his time servicing his existing clients’ policies. If you’re an agent at a captive agency like State Farm, you may also need to help service clients who have a State Farm policy but are not even in your own book.

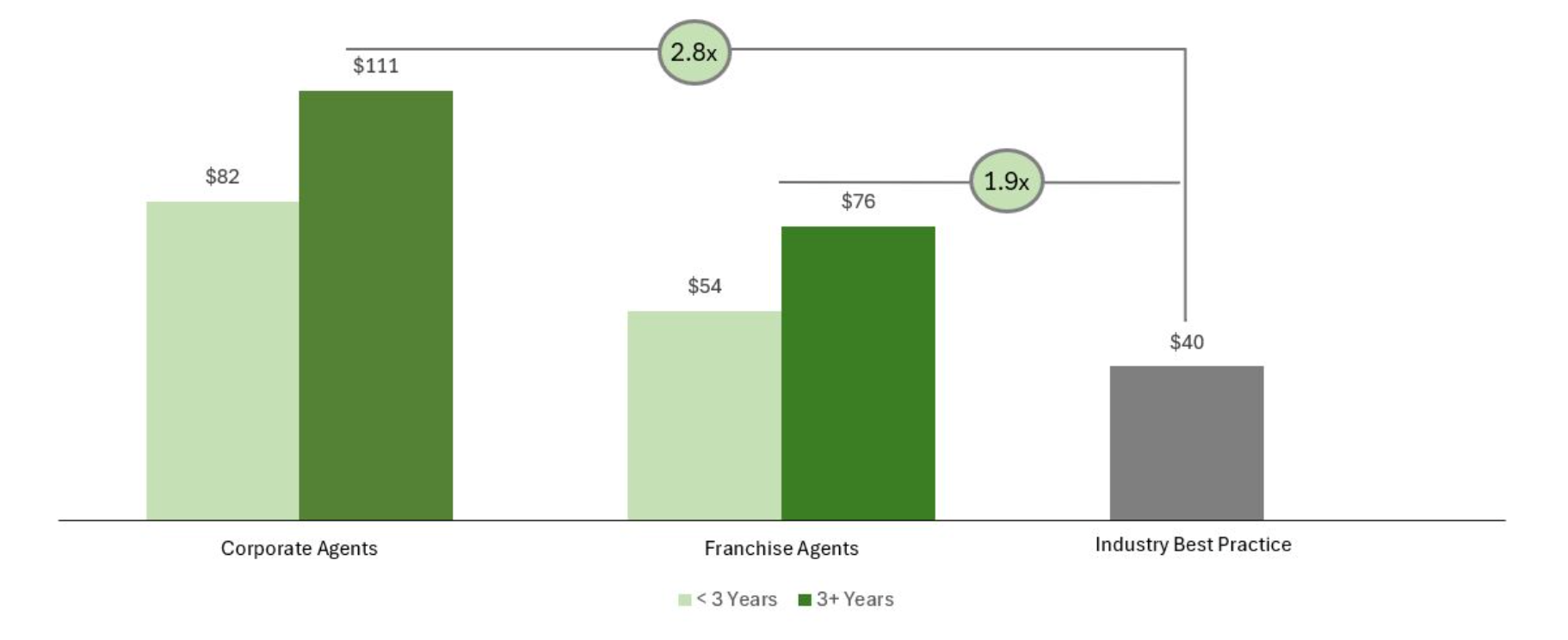

It turns out that this separation or comparative advantage strategy doesn’t just make sense in theory, it actually works. Goosehead franchise agents are significantly more productive than the industry average:

While having producers focused on sales is best for business, the service piece cannot be ignored. Service is an important part of the relationship with the consumer, and the better the service, the better the retention.

Service at Goosehead is centralized, meaning it has P&C licensed corporate employees who handle the servicing of all policies in the Goosehead system, including those at the franchised agencies. If consumers have claims, policy changes, questions, payment processing, etc., they are handled by the service team. Their personal agent who sold them their policy may guide them and answer some questions, but ultimately the service team handles the load.

To evaluate the performance of the service function, we can look at client retention rates. Client retention at Goosehead in 2024 was 84%, which Goosehead believes is the best in the industry. They also talk about their Net Promoter Score (NPS) being higher than almost any consumer brand in the 80s to low 90s, but I am skeptical on how NPS scores are obtained, how meaningful they actually are and how they are touted by companies. There is a deeper story to how service at Goosehead is actually working (read: it has been bumpy), and we will get to that in Part 3.

To sum up the separation of sales and service model, the model is, “you’re great at selling, so that’s all I want you to do. We’ll take care of the service.”

As a result, the Goosehead model is one that’s geared for growth. Agents’ biggest incentive is to sell new business policies, because they don’t have to divert time and attention to service. Freeing up the burden to service the book of business lets agents use the vast majority of their time and energy for new business. This is also important for larger books of business, because the larger the book, the greater the need to service policies, which is a significant cost of time and money.

Compared to the other agency ownership offerings in the industry, the sales and service separation model is the surest way to grow a large book of business in a relatively short amount of time

New business generation via home sale referral partners

If you are an independent insurance agent, you might want to have a coherent strategy to generate new business.

One strategy, which is used by the captive agents and has been done since before the internet era, is buying leads. Leads are contact info of people who are likely currently shopping for home insurance. The problem with buying leads is it costs a lot of money and conversion rates are low. This is a contributor to the low bind rates. Plus, being solicited is not a pleasant customer experience.

Another strategy is building a referral network. You could ask your existing customers to tell their friends and colleagues to come to you for their insurance needs. You could build relationships with local financial advisors, accountants and attorneys to refer you to their clients, but their clients are not necessarily imminently in the market for insurance. The best referral relationships are real estate agents and loan officers who refer you to their clients during the home buying process. The reason these are the best referrals is that there’s no doubt that there’s an imminent need for insurance on a new home closing.

Importantly, loan officers and real estate agents do not get paid unless their transactions close. No deals, no comp. Each of these referral partners has an incentive for a deal to get done, and therefore they have an incentive for the insurance to get done without a hitch (remember, insurance is required to buy a home). If you’re an insurance agent known for getting the insurance done right, with adequate coverage and with speed — in one word, reliable — these referral partners will come to like you and send you a lot of business.

These are the referral partners the Goosehead model focuses on, and it makes the lead generation process simple, effective and cost efficient.

While referral partners are the ‘who,’ another dimension is the ‘what.’ By that I mean the product you lead with as an agent. For personal lines, it turns out it makes sense to lead with home insurance. This means that to find new business, you find opportunities to sell a home insurance policy. If someone owns a home, it’s likely they own a car. This isn’t true the other way around. This isn’t really a blinding insight that Goosehead has and it seems to me that this is generally the way most agencies sell, but it is worth mentioning to understand how the industry works.

Bundling also tends to make the customer relationship stickier, so the more policies you bundle, the longer your customer sticks with you. Home by itself is stickier than auto by itself. Bundling is obviously good for business.

Technology to support sales and service

If you’re an insurance agent, what would you rather have?

- Multiple agency management systems you have to switch between, some outdated computer systems and mainframes, multiple places you have to go to quote polices, and no relevant real-time go-to-market data.

- A single tech system, built on the cloud so you can access it anywhere with a laptop, containing everything you need to do your job, including real-time go-to-market data to help you find new business.

It’s a rhetorical question! Other key benefits of Goosehead having built structure #2 for their tech platform:

- Speed. With one platform, everything the agent needs is in one place. Customer data collection from potential new policy owners can also be collected more quickly, and in fact Goosehead’s system enables agents to quote policies with fewer data points.

- Real-time closing and productivity data to enable better lead generation. This is primarily data of loan officers by name in each local area and the amount of loans they’ve recently been closing — this is a list of referral partners for agents to target (it is all actually public data, but the system pulls and organizes it cleanly). The data is real-time, so it updates with the market. Also, once an agent in the system builds a relationship with an RP, that RP is removed from the visible database as to avoid hyper-competitiveness among Goosehead agents.

- Rater / policy comparison tool called Aviator that enables agents to pull multiple quotes for a potential customer, and does it quickly. Goosehead was not satisfied with the off-the-shelf solution, so it built its own.

Goosehead has built and continues to build other tools in its proprietary tech stack:

- Quote-to-issue, which enables agents to quote and bind policies on the Goosehead side rather than sending a quote to the carrier for approval. This requires the Goosehead tech team to work with the carriers’ tech team to integrate their back-ends.

- Digital Agent, which is a consumer-facing quoting tool so consumers can get quotes for themselves, which then becomes an actionable lead for an agent. Digital Agent 2.0 aims to enhance quoting to better match insured risk to carrier appetite and to remove human capital bottlenecks where it makes sense.

- Consumer-facing mobile app, which was recently rolled out at the end of 2025. This provides a Goosehead-branded mobile-native experience for consumers to view and manage their policies all in one place, including the ability to shop for renewals.

Goosehead views its overall tech platform as a competitive advantage, and it employs a large in-house technology team (development and engineering talent) to keep widening that advantage. We’ll aim to revisit this in Part 4.

Summing it up

- Having choice is the better way to buy home insurance

- Home insurance is not as straightforward as auto insurance, so it helps to have a human agent and their local expertise

- Goosehead is an independent agency that:

- pioneered the idea of separating the sales and service function

- is geared for book of business growth

- delivers a win-win-win for buyers, agents and carriers

- takes technology seriously