Part 2: Personal Lines P&C Industry Primer

Part 1 provided an overview of the basics of the Goosehead model. This Part 2 is an industry primer on personal lines P&C.

Personal Lines P&C Basics

Personal lines property & casualty (P&C) primarily means insurance policies purchased by individuals to protect property risks and personal liabilities. Auto and home (HO) are obviously the most prevalent, so “personal lines” generally refers to auto and home. Coverages like renters, flood, earthquake, umbrella, etc. are also personal lines P&C but represent a smaller portion of the overall written premium in personal lines.

Auto and home insurance are non-discretionary purchases — you must buy them. If you drive a car, you’re required by law to have auto insurance (unless you’re in New Hampshire where you still have to prove you can self-insure). If you want a mortgage, your lender will require you to have home insurance (the loan is secured against the house, which is effectively their asset and they want it insured). A non-discretionary product means there will be insulation against macroeconomic downturns that weaken consumers.

Auto policies typically have 6-month policy periods and homeowner policies typically have one-year policy periods. Policies are repriced at each renewal term. Having the ability to reprice policies on a relatively short cycle enables insurance carriers (carriers meaning the underwriters who hold the risk and write the policies, such as State Farm, Progressive, GEICO, etc.) to quickly adapt to cost inflation or loss events.

Thinking simplistically, underwriting an auto policy is fairly straightforward relative to a homeowners policy:

| Auto | Home | |

|---|---|---|

| Primary Source of Risk | Driver | Geography |

| Loss Claim Dollars | ~45% Physical ~55% Liability |

~97% Physical ~3% Liability |

| Value of Asset | <$50K | >$500K |

| Underwriting Data Points Required | 30–50 | 100–300+ |

| Variability of Coverages | Low/Standardized | High/Customizable |

| Variability of Quote Pricing | Low | High |

| Risk of Underinsurance | Low | High |

| Variability of Carrier Appetite | Low | High |

| Value of Agent Advice | None to Low | Medium to High |

Market Size and Growth

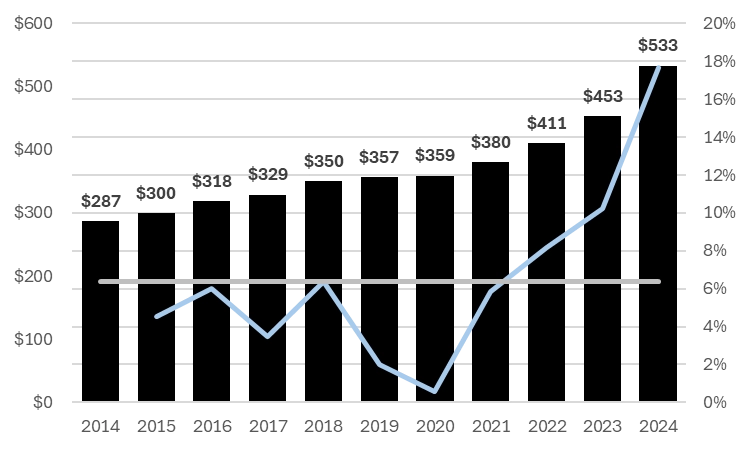

Annual written premium in personal lines is over $500 billion annually, growing 6.4% per year since 2014. Premium is the amount paid by the insured to the insurance carriers / underwriters. At the market level, total premium growth is a function of a) change in policies, fundamentally supported by population growth, and b) premium/rate growth per policy, or pricing. At any given insurer or agency’s book, premium growth is a function of a) policy / client retention, b) amount of coverage and c) pricing.

Annual Personal Lines P&C Written Premium and Premium Growth

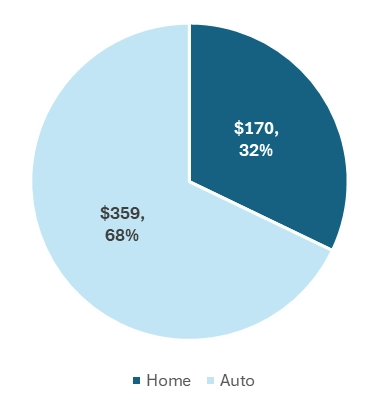

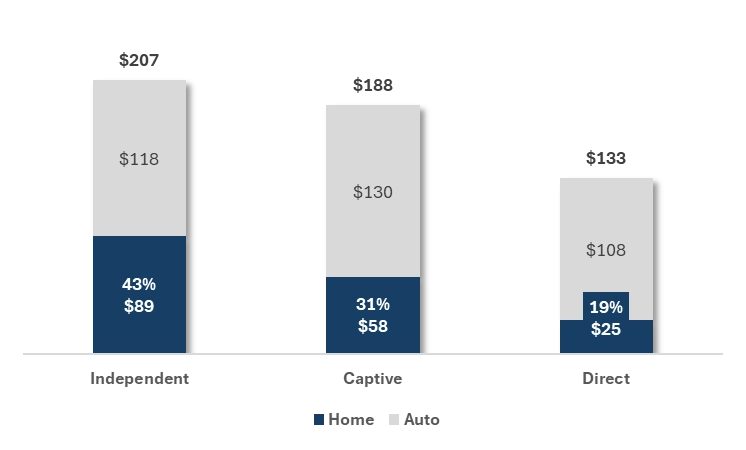

Auto is ~70% of personal lines premiums whereas home is ~30% (there are many more cars than homes, cars are operated by humans, and cars move around). The chart below shows the split 2024.

Total written premium has risen about 6% per year in the last 10 years. More on the pricing component of growth later, but annual rate growth in HO has structural components supporting growth in excess of base inflation: construction, repair and replacement costs outpacing inflation; increasing loss exposure from “secondary” perils; and rising wealth and asset values.

How Many Homeowners Policies Across the $170B Premium in the US?

The total single-family detached and attached housing stock in the US is about 100 million units. Several methods of estimating total policies in force on these homes triangulate around 80 million, factoring in the uninsured penetration of the homes that do not have mortgages.

It’s also important to understand the number of housing transactions every year because a housing purchase transaction is the strongest catalyst for a new homeowner’s policy.

The 15-year average of existing home sales is about 5 million per year, and in 2025 that number was 4 million, so the current pace is about 20% below the 15-year average. The consensus view is that there’s a housing shortage in the mid-single digit millions of homes in the US that would take at least a decade to correct, because the pace of new construction, which is 550k-600k annually the last 15 years (depressed versus 1M+ pre-GFC), needs to eat into the shortage/gap while also absorbing new household formation every year.

The problem, however, has been high interest rates, which have created a lock-in effect for homeowners who don’t want to give up their low rate by moving into a new home, holding housing inventory low.

Drivers of Written Premium Growth

Basic underlying drivers of volume (more policies or more coverage)

- Household formation driven by population growth

- Rate of homeownership

- Additional coverage (e.g., higher limits, flood, etc.)

- Second home / vacation home ownership

- Declining uninsured rate

Catalysts for single-family housing transactions which are catalysts for new policies (not necessarily new in net terms because policies move among carriers)

- Increase in existing home sales

- Increase in housing starts / new home sales

- Decreasing interest rates → increase in mortgage refinancings

Basic drivers of price/premium (higher price, more insured risk)

- Replacement cost of assets insured, largely driven by inflation (building materials, labor, tariffs, shipping costs, etc.)

- Increasing exposure to risk, not only primary perils like hurricanes but secondary perils like severe convective storms and wildfires; population growth/migration to higher risk areas like Sunbelt and Florida

- Increasing home values (weaker driver than replacement cost)

- Cost of reinsurance (ebbs and flows with market cycle, but with rising risk over time, this is structurally higher; a derivative of increasing risk exposure listed above)

- Aging housing fleet, which is more vulnerable to loss

- Social inflation, increasing claim litigation

- Regulation-caused inefficiencies such as a lack of private market admitted market insurers and long rate approval timelines (higher risk of rate inadequacy, which in turn causes larger catch-up rate increases); culprit states lately are CA and FL

- Increasing share of homes built with lesser quality and cheaper materials; exacerbated in times like now when the largest homebuilders are facing low demand, and in turn, pricing and gross margin pressure

Severe Convective Storms (SCS) and Wildfire Driving Loss Trend, Structural Rate Repricing

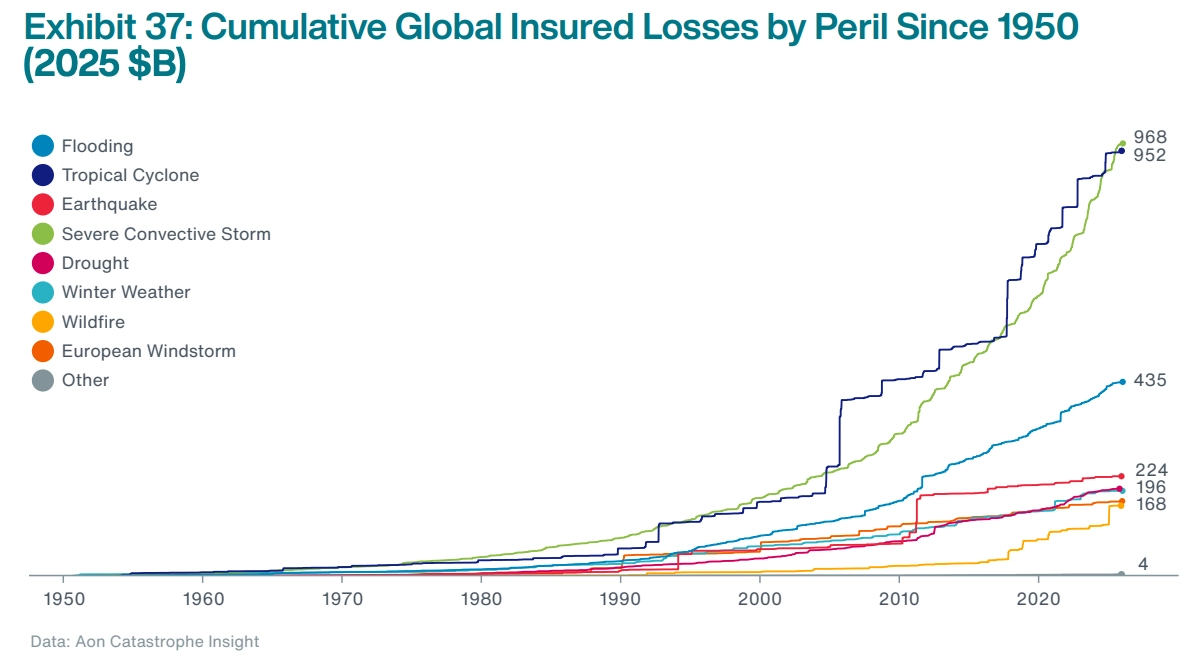

The single-biggest exposure growth category in US personal property is SCS. As of 2024, according to Munich Re, the 5-year annual insured loss from SCS was $2.5B in the early 1980s, but the last three years have produced insured losses north of $50B annually. This is a 20x increase. SCS is no longer a “secondary peril,” it is now a primary peril.

Wildfires are also responsible for an increasing share of insured losses. The Palisades ($33B economic loss) and Eaton ($25B economic loss) fires in California in 2025 were the “costliest fires of the modern era” and were the top two loss events globally in 2025. For comparison, the infamous Paradise fire in 2018 had an economic loss of $17B in 2025 dollars.

The fascinating chart below tells this story; you see both the growth with SCS and wildfires, and you see that SCS is now the leading peril.

While climate change is a component of increasing losses from SCS, the primary driver is the increasing value of insured assets in harm’s way. This is driven by more people moving to vulnerable risk areas, and their wealth and home values rising. This altogether is referred to as exposure growth.

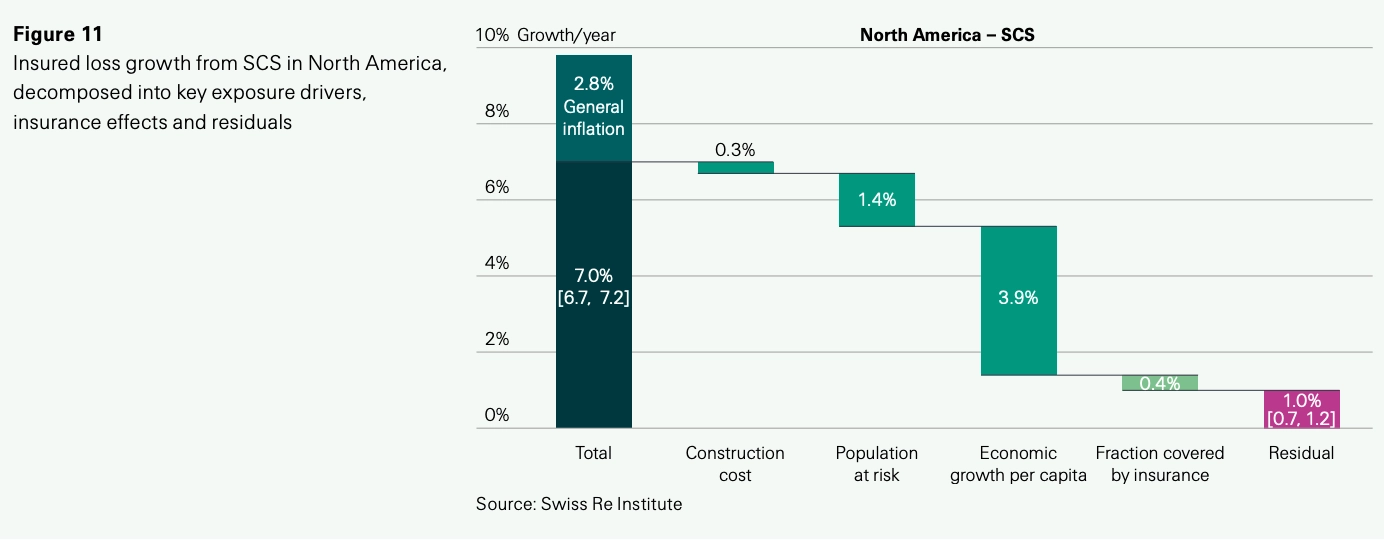

Swiss Re estimates that about 80% of the growth in insured SCS loss is attributable to exposure growth (below, construction cost in excess of general inflation plus population at risk plus economic growth). The residual component is where the climate risk component sits. The takeaway is that insured losses from SCS are growing at 7.0% absent of inflation, of which 5.6% is from exposure growth. This must be reflected in insurance premiums as carriers reprice for this risk.

In contrast, the residual component for wildfires explains 60% of the non-inflation growth, suggesting that underlying climate change drives most of the loss and rate repricing from wildfire risk.

Market Structure: Shifting Distribution Trends

There are three basic ways that personal lines insurance is sold:

- Direct from the carrier: Progressive and GEICO are most prevalent in direct. Consumers go online to Progressive or GEICO’s website to buy a policy directly.

- Captive agent: State Farm pioneered the captive model. Consumers buy policies from their local State Farm agent, who sells only State Farm policies. Certain other insurers use the captive model, the most prominent being Allstate and Farmer’s.

- Independent agent: An independent agent offers policies from multiple carriers with which he/she is appointed. Carriers must appoint licensed, independent agents who are effectively committed to bringing quality clients to the insurers; not anyone can just call up Progressive and start selling insurance.

It is informative to look at premium by channel, for each of home and auto.

2024 Personal Lines P&C Premiums by Distribution Channel

Given the nature of the product, it is not surprising that the independent channel commands the greatest share of home insurance, because home is a more complex product that benefits from an informed expert involved in the sale process (both for the insurance policy itself and for the home closing transaction). Likewise, direct commands the greatest share of auto as an auto policy is more commoditized.

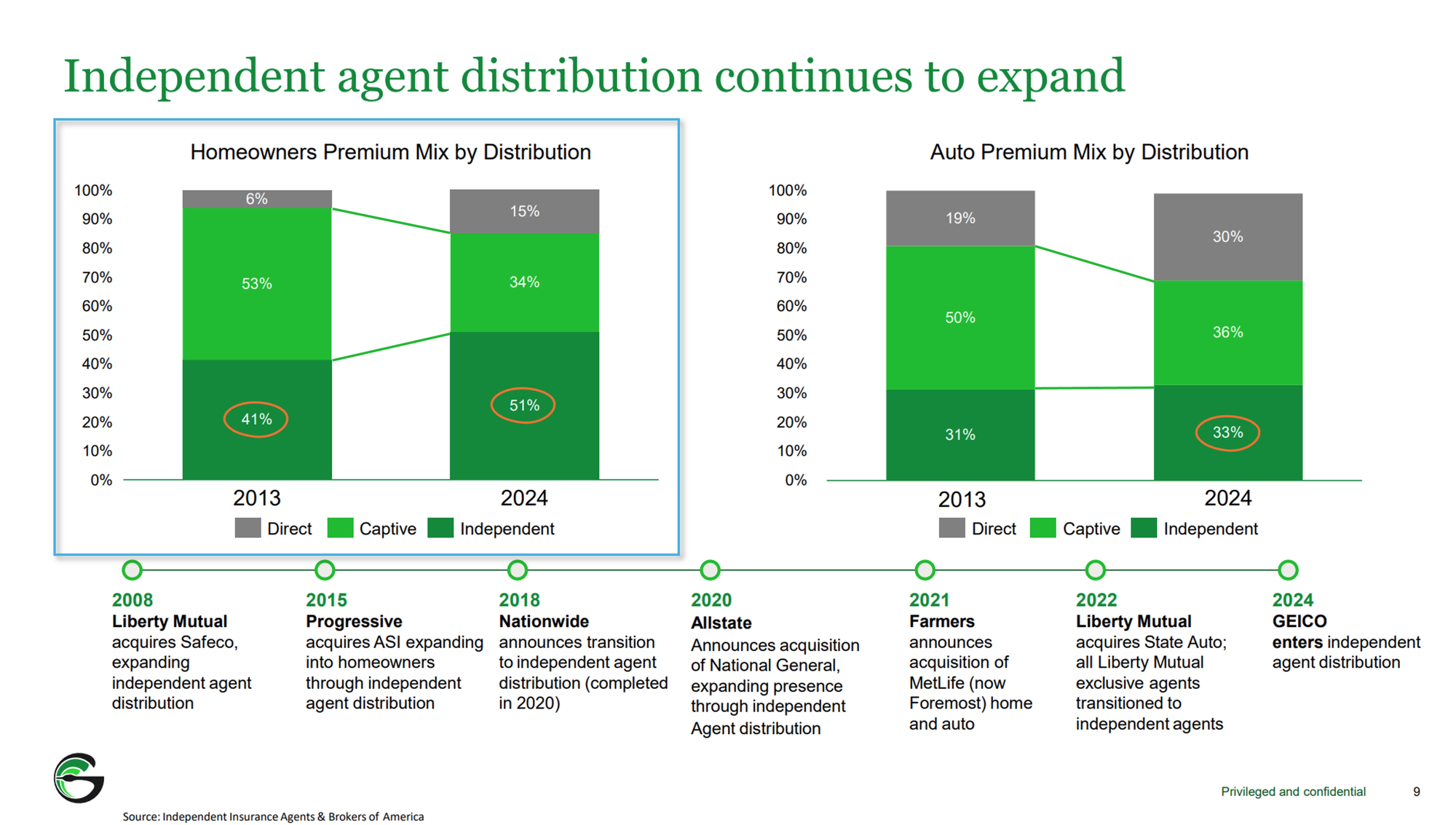

It is also informative to look at how distribution has trended over time (boxes and lines added on top by me).

This depicts the most impactful structural dynamic in the personal lines industry, in my view. In the last 10 years, the way personal lines insurance is bought has been changing significantly. Within home:

- Captive has shed nearly 40% of its share — 19 points of share — to the Direct and Independent channels

- Direct has picked up 9 of those points. This is arguably attributable to the general trend of more consumer transactions moving online, similar to the physical retail → ecommerce trend. Consumers have become increasingly comfortable moving more and more of their transactions online or to their phones

- Independent has picked up 10 of those points. This is arguably attributable to a better consumer experience; that is buying insurance with choice coupled with a knowledgeable expert, supported by tech-enabled tools. As independent agencies grow and gain more carrier appointments, they are able to offer more choice at more points in time, further reinforcing their value proposition. There may be a long way to go on this path as the independent channel remains fragmented, and like other industries, scaled distributors command increasingly larger economies that will make it more difficult for mom-and-pop agencies and captive carriers to compete

- Direct insurers have increasingly moved into the independent channel to broaden their customer acquisition funnel — these include the largest carriers, with the most notable moves listed at the bottom of slide above: Liberty Mutual, Progressive, Nationwide, Allstate, Farmers, and most recently, GEICO. GEICO has over decades touted the low-cost competitive advantage of writing auto insurance direct, but I believe came to the realization that in order to be competitive in winning share and competing with Progressive, it needed to open itself to the agency channel to access consumers who are increasingly looking for choice

Why is homeowners insurance a product that’s more suited for the independent agency channel than auto, and where the shift to independent agent distribution is more potent?

- Product complexity — insuring a home is relatively more complex than an auto, often requiring 100-300+ data points. There is also a wider variety of relevant coverage options. This means that obtaining and understanding a HO policy is more difficult than for autos

- Pricing variability — quotes for home insurance can vary by thousands of dollars, making independent agent advice more valuable

- Value of asset — homes are often the most valuable asset in a consumer’s net worth, multiples of their cars, so adequate protection is more important

- Risk matching for carriers — locality and risk varies widely for home versus auto, and independent agents with local expertise and customer access provide value to carriers looking for or avoiding specific risk profiles. Agencies act as demand curators for carriers, in a more efficiently decentralized way than the carriers could do on their own

Underwriting and Distribution are Fragmented

Carriers / Underwriters

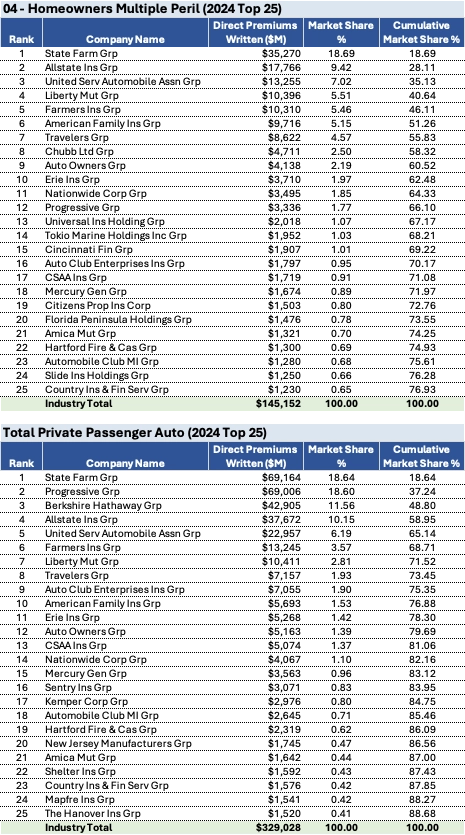

On the carrier side, while there are the handful of about eight majors, the tail is long and there are a large number of sizable carriers. More specifically, there are more than 450 carriers in personal lines, of which 160 have more than $100m in annual written premium.

Homeowners is more fragmented on the carrier side than auto with 62% of premiums written by the top 10 versus 77% for auto.

In homeowners, it’s notable that 3 of the top 5 are captive underwriters (State Farm 1, Allstate 2, Farmers 5). This supports the idea that home buyers and homeowners prefer to buy home insurance with an agent’s presence, but more importantly it shows that the shift away from captives has a long runway. I would expect to see the carriers in the middle of the table above continue to climb up.

As carriers consolidate and/or become larger, they should naturally prefer to deal with increasingly scaled distributors/agencies. This dynamic is referred to as panel consolidation and has played out in the commercial insurance market.

Distributors / Agencies

In distribution, the lines get a little blurred on written premium when distinguishing between personal lines and commercial lines. Nearly all independent agencies sell both commercial and personal lines, and the largest agencies overwhelmingly index to commercial lines. Businesses are more complex to insure, need more insurance and are typically even stickier than consumers (though consumers can also be sticky with their policies; I’d bet that often you will hear, “I’ve been with GEICO for 60 years,” just ask your older family members). There are also more coverage lines within commercial, which enables agencies to carve themselves a sufficiently sized niche.

The one major exception to the dual commercial/personal focus is Goosehead, which is a multi-billion-dollar written premium agency almost exclusively focused on personal lines. This is intentional on their part. Closer Goosehead competitors who do sell personal lines usually have sizable commercial businesses; in other words, there’s not an intentional and narrow focus on personal lines. These include agencies like Alliant/Confie, TWFG, Baldwin, HUB and Acrisure.

Within distribution of personal lines insurance, there are a few distinct business models.

The first is the “standard” full ownership model. The company owns all of the individual books of business and its employees are the licensed agents.

The second is a network or alliance model. These are networks of independently owned independent agencies, with the main value proposition of the network being that it provides carrier appointments. In other words, they help smaller agencies get off the ground faster by giving them access to carriers. They often also offer other services and support like access to technology. The agencies own the books of business, and the agency gets a relatively modest percentage fee/commission on premiums. The large ones here are FirstChoice (a MarshBerry Company), SIAA, Keystone and Ironpeak.

The third is a “franchise” model. A franchisor brand provides an out-of-the-box solution to a licensed agent. The solution includes carrier appointments, a full technology stack, training (more valuable for agents entering the industry, still valuable for agents entering a brand from another brand) potentially a service support function and other ancillary services. The agents own the economics of the book of business.

“Franchise” here I think is a bit of a misnomer compared to what we’d normally think about as a “franchise,” like a McDonald’s or a Planet Fitness unit. For one, the royalties in the insurance agency models are on the surface much higher than the typical single-digit royalties you’d see in restaurants, and there is not a significant upfront investment. That there’s not a significant upfront investment tends to attract franchise operators that look more like independent contractors than investors and business owners. I think the more useful comparison is the real estate agent joining a partner firm like Century21, Compass, etc. where they share transactional economics.

For the independently owned agencies, it is important to observe that it doesn’t take much capital to start an insurance book, selling insurance is a fairly accessible game to learn and the barrier to getting licensed is not high. So it’s likely that any given time, there will be an ample number of willing agent-owners starting new books of insurance. Which type of model they choose to wield has a large influence in determining their fate.

Benefits to Scale for an Independent Agency

The key benefit for an independent insurance agent in having access to a scaled distribution platform is carrier appointments. A large independent agency or network like Goosehead or SIAA, because of the amount of business it provides to carriers, and because of its level of sophistication, can command appointments with a large chunk of the 400+ personal lines carriers. By belonging to one of these organizations, the agent also has instant access.

Not having access to a sufficient number of appointments would render the independent agency model moot. If you’re an agent appointed with only two carriers, you’re not offering your clients choice.

Another major benefit of scale is the ability to invest in and improve technology. Technology is central to the agent and consumer experience, enabling general ease throughout the purchasing process, and importantly, speed.

From the carrier perspective, having fewer and larger independent agents bringing in business is much better than plentiful and smaller — there are fewer constituents to manage, sophistication is higher, and technological innovation benefitting the carrier happens faster.

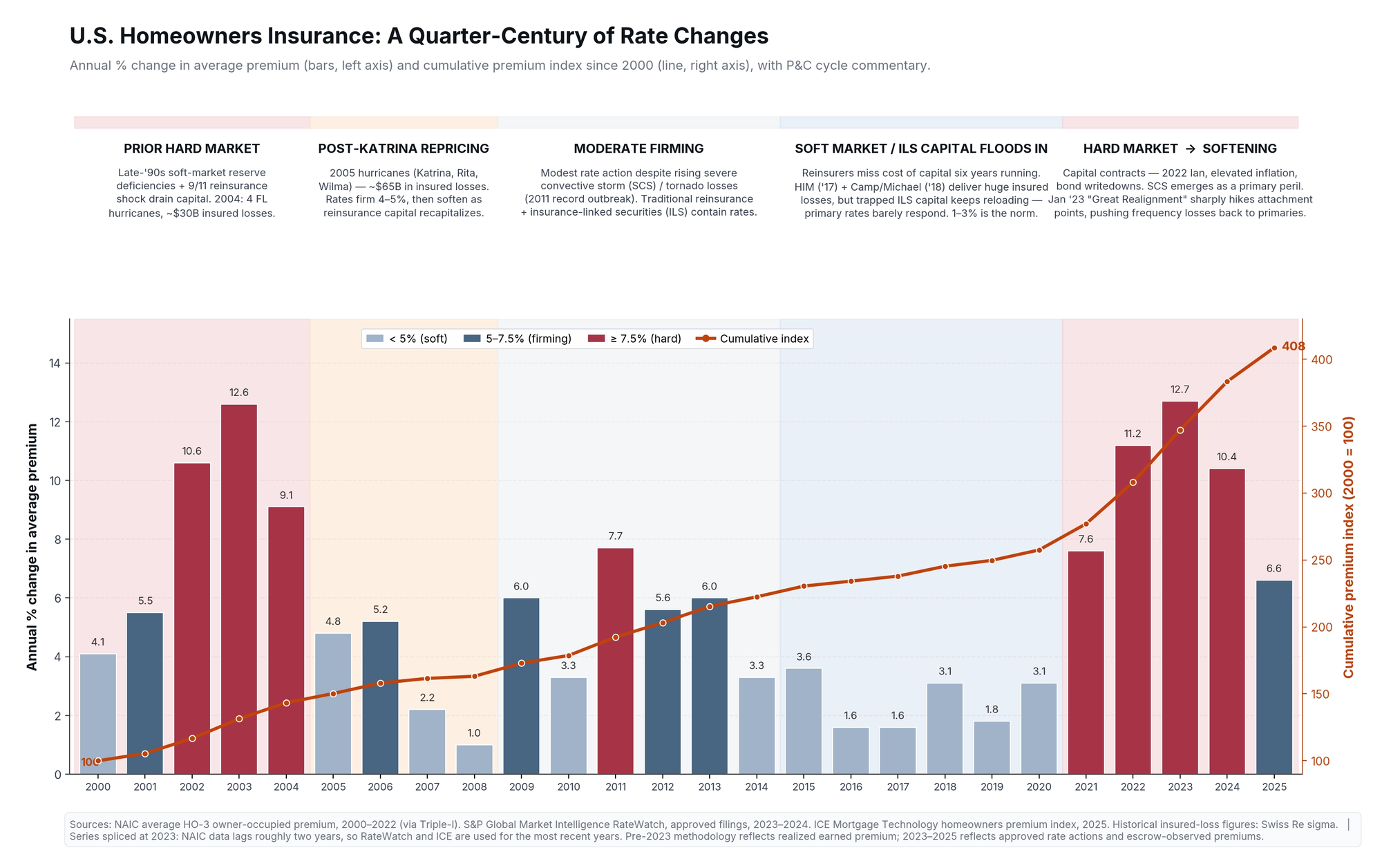

Homeowners Insurance is Currently Easing Out of a Hard Market

In insurance, it’s important to understand whether the market is currently hardening or softening. Hardening refers to rising rates, associated with less insurer capital at work. Softening refers to decreasing rates, associated with an increasing abundance of capital.

It works as a cycle because hardening and softening each effectively cause the other. An abundance of capital, observed by insurers’ willingness to to place policies and therefore a creation of ample supply, breeds competition, driving down rates. When rates are driven lower to the extent that they are insufficient to cover losses from loss events like natural disasters, insurers start to become less profitable or unprofitable, do not earn attractive returns on capital, and capital leaves the industry. This in turn leads to higher rates, insurers rebuilding reserves, and a lack of willingness by insurers to place new risk; in other words, a lack of supply leading to a hard market. When rates are driven higher relative to losses incurred, insurer profitability and returns on capital become attractive, so capital returns to the industry, initiating a soft market.

There are also longer-term structural changes that can affect the rate cycle, like a secondary peril such as severe convective storms (SCS) becoming a primary peril.

As the chart of the homeowners insurance rate cycle below depicts, 2021 through 2024 has been a historically acute and persistent hard market. This was driven by a lengthy soft market from 2013 through 2020, and a variety of factors in 2021 through 2024: elevated inflation driving up replacement and repair costs of homes, higher interest rates driving losses on insurers’ bond assets, a slew of insured loss events including higher losses from SCS and structural repricing in the reinsurance market.

Easing started last year, which is expected to continue this year. This means homeowners’ premium rate increases will be moderating.

Note that according to the data depicted in the chart, there has not been a single year since 2000 where rates declined in homeowners (for comparison, this is not true for personal auto, where 2005 through 2009 showed rate declines in the 0.5% to 2.4% range).

Thoughts on Personal Lines Insurance and AI

A primary industry narrative at the moment is that AI could disrupt and disintermediate insurance distribution. This was caused by the release of a few ChatGPT-linked tools in the second week of February:

- Tuio, a startup insurance MGA in Spain launched in 2021, released a ChatGPT app that apparently enables customers to get a quote from Tuio natively inside ChatGPT. It is not a comparison tool enabling a customer to see quotes from other carriers

- Experian launched a ChatGPT app (the consumer must install the app) that enables consumers to see price ranges for auto insurance based on a ZIP code. It then redirects them to Experian’s existing online marketplace, where it is effectively a broker and collects commissions as a licensed agent. It essentially resumes the quoting process on that web page, asking questions that are required for a true, non-preliminary auto insurance quote

- Insurify, an online marketplace that is licensed to sell policies, launched a ChatGPT app (the consumer must install the app) that enables consumers to see price ranges for auto insurance. based on a ZIP code. It then redirects them to Insurify’s existing online marketplace, where it then asks the more detailed questions to provide a quote as a consumer already would on its web page. In other words, it seems to be the same thing as Experian’s product

Note that the two US products mentioned above are for auto insurance, not home insurance.

The developments above, in conjunction with similar narratives like “software is in trouble because of AI,” caused selloffs in insurance brokerage stocks.

Was this kind of narrative swirling at the turn of the century with the proliferation of the internet? Indeed, the same narrative was in play! The conclusion of a 2003 academic paper “Insurance Distribution Channels: Markets in Transition” — note it is 2003, about four years into the dot com ‘boom’ — debunks the then-narrative:

Our analysis makes it clear that the early predictions of widespread adoption of the Internet as an insurance marketing channel were inaccurate. Insurers are using the Internet-led channel in a support rather than in a direct sales capacity. Also, the experience of online insurance brokers suggests that customers are less likely to sign up for insurance online, but instead use online sites to receive quotes from several insurers or to get identification cards and certificates of insurance quickly (Ha, 2003).

Given the disintermediation that has occurred in other industries (e.g., travel), the question then arises as why the insurance industry experience has been different. We suggest that perceived product complexity in part explains the very low levels sales of insurance products through the Internet- led channel. Some have suggested that airline tickets and insurance policies both are commodity types of purchases. As such, consumers would use price as the purchasing criteria. It seems clear that the complexities (perceived or actual) associated with the insurance contract make it a distinct type of purchase in the minds of many consumers. As noted earlier, product complexity also explains differences in adoption patterns between different types of insurance (e.g., higher adoption rates for personal auto insurance than for commercial insurance).

How Has Personal Auto Been Sold Since the Introduction of the Internet?

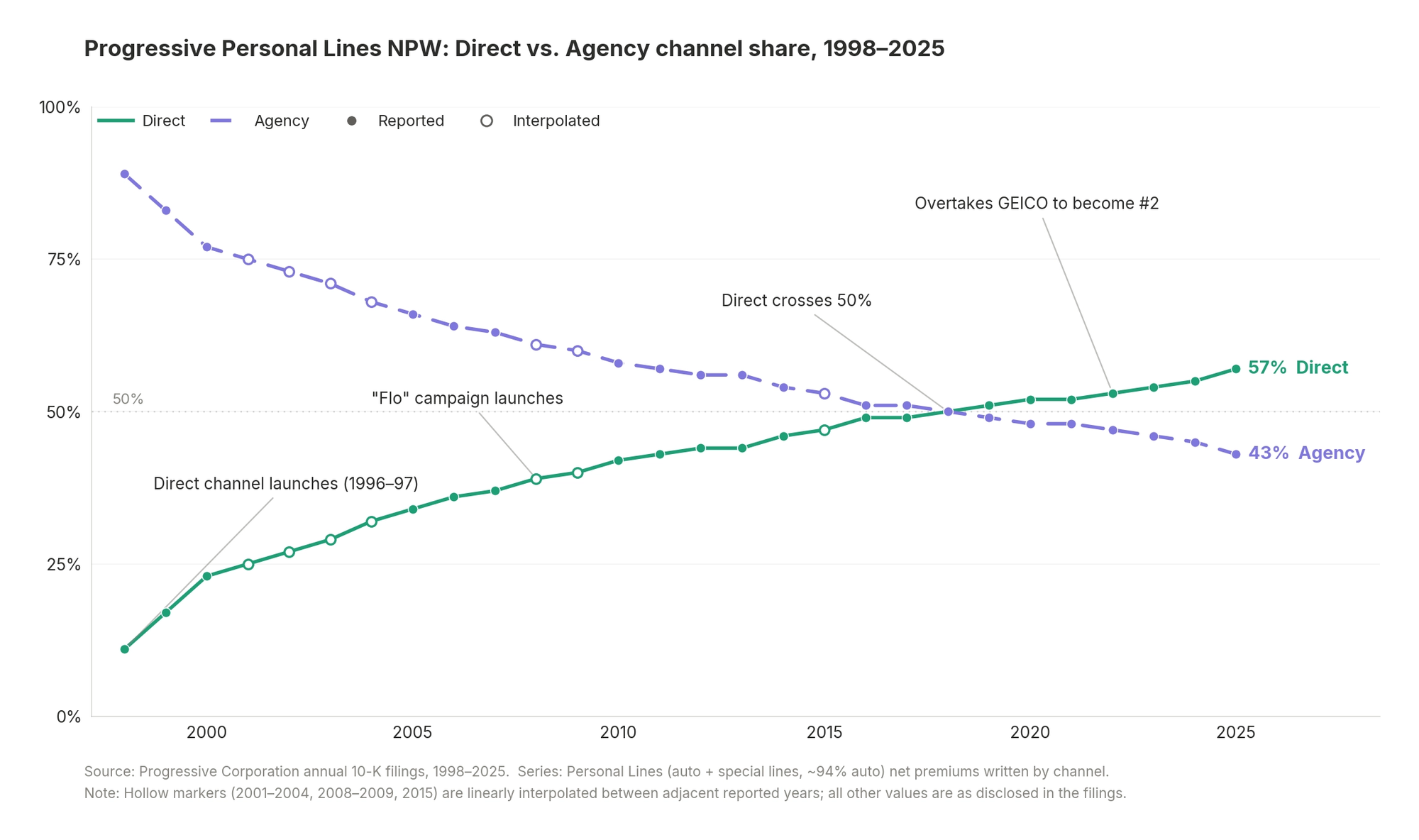

Progressive was the first insurance carrier to offer online binding in 1997, has invested heavily in its direct and digital offering and is the largest writer of personal auto insurance in the US today, making it a suitable case study. Below is a graph of its premiums written direct and through agencies.

The takeaway is that even for a leading insurer focused on growing its direct channel, it took 21 years (1997 to 2018) for direct to eclipse agency written premium. The growth of share to direct at the outset was larger and more of a step-function, but it has been a slower build since then.

Why has this been the case? There are probably several reasons for the slower-than-perceived pace of direct binding adoption in auto policies, including:

- Insurance is one of the stickiest products consumers purchase, and annual catalysts for buying a new policy represent a fraction of total policies; consumers don’t often have a reason to change their policy

- It’s expensive for direct carriers to acquire direct customers, somewhere in the $1,000 per customer area. The reason is TV advertising and buying leads are both expensive. Relative to the commission paid to an agency, which tends to have higher quality customers (more assets, more likely to bundle, lower risk), acquiring customers for the direct channel may not actually be much cheaper relative to lifetime customer value

- It takes a long time for consumers to change engrained behaviors; insurance policies were for a long time purchased via humans, and it is easier to leave a policy be and pay it every year on auto-renewal. If a policy was originally purchased via an agency, the renewals continue to go to the agency

- Some consumers want someone else, an agent, to do their insurance work for them. It is a service, just like having taxes done, going to a restaurant meal, having the house cleaned, etc.

- There’s perceived complexity by the consumer for an insurance policy, and they want to talk to someone who understands it

- Insurers like Progressive don’t want to completely alienate their independent agency distribution channel, as doing so would terminate the relationship, albeit indirect, with a huge swath of its high-quality policyholders

Outside of Progressive, looking at the entire industry, the JD Power insurance shopping survey for 2025 observes that 47% of consumers bind their auto policies online today. So the industry as a whole has not yet reached the majority mark of online binding, 28 years after the first auto quote was bound online. 35% of consumers still purchase their auto policies with an independent agent today, and 53% doing so with a human.

Will AI technology accelerate the number of auto policies bound online?

Like the internet with search, AI is a tool for gathering information quickly. LLMs do so in a higher quality way, digesting much more information in a short period of time. The LLMs therefore draw a lot of eyeballs. But in the context of buying insurance, AI so far seems to lack any fundamental change in feature or additional advantage compared to the already-in-place quote shopping tools that consumers have had online for almost three decades. AI probably enables consumers to more easily learn about how their auto policies work and when it might make sense to shop for a new policy. But the actual binding process, including the personal details required to produce an accurate quote that can be bound, is not suddenly fundamentally changed. AI and LLMs are simply another digital entry point for consumers to being their insurance shopping, and in fact, today’s crude LLM apps take the consumer to the insurer’s quoting website.

The biggest value-add from a scaled independent insurance agent is the offering of choice, because it has relationships with carriers. Without those relationships with the carriers, choice goes away. The value of an independent agent is in those relationships, not in the medium with which consumers can bind their own policies.

Maybe the LLMs, given the vast amount of usage and eyeballs they command, could over time lower customer acquisition costs for carriers selling direct, making it increasingly attractive versus independent agencies. If that were to happen, maybe independent agency commission rates would have to come down. For this to be true, there has to be something fundamentally different that AI offers compared to today’s online marketplace / lead generator websites, which consumers are directed to from Google. I struggle to see what is fundamentally different with LLMs here versus the existing online offerings.

HO Insurance is More Complex than Auto, Less Suited to Unadvised Purchasing

As the 2003 study hypothesized, product complexity, perceived or actual, could be a primary reason that personal lines insurance maintains a presence with independent agents.

The complexity of an insurance policy, in basic terms, is driven by the uniqueness of the risk, the number of perils and coverages, correlation of risk, risk data availability (higher frequency of losses means more data), loss tail length and reinsurance integration.

An auto policy is fairly standard on all of these dimensions: the risks are fairly homogenous / not unique (a 2021 Tesla Model Y is a 2021 Tesla Model Y; whereas two homes in the same neighborhood could have dramatically different risk profiles despite common geography), the peril is collision-driven, risk correlation is low (car accidents are independent events unlike a hurricane wiping out an entire area), data availability is high, tail length is low (the loss is known shortly after the accident) and there’s very little reinsurance integration.

Another way to view this is that auto insurance is basically commoditized, whereas home insurance is not. Home introduces more perils and variables and coverages that make each home a relatively more unique risk. These de-standardize and de-commoditize the insurance.

The more complex the insurance product, the more likely it is to be sold with agent advice. This is common sense — the consumer is uninformed and a consumer doesn’t want to learn how to become an insurance agent himself. Nor does he want to spend the time with the data capture and entry, shopping around for quotes, and understanding differences in coverages for the many variables required for home insurance.

In addition to offering choice among several carriers for a given home policy, an agent can offer advice on coverage options, and an agent in the flow of writing policies in a given local area understands which carriers are offering which coverages at which prices. Carrier appetite shifts, and prices can move at certain carriers more than others. An agent who can navigate this is valuable not only in terms of quality of coverage and price, but in time saved for the consumer in the buying process. Particularly in a home buying transaction, speed is valuable.

All of this is to suggest that because HO insurance is a relatively complex product compared to auto, it is less suited to an automated purchase process that an LLM may one day be able to handle. Even auto policies took 28 years to get to the ~50% mark for binding online. People want someone else to handle their home insurance — it’s easier, faster and better. And relative to purchasing direct, there is not a price gap, or at least an obvious price gap. The consumer doesn’t pay more to buy an HO policy through an agent. Even it it did come with a noticeably distinct fee, the fee may still be worth the time and headache saved.

Current Working Hypothesis and Possibilities on the HO Insurance Buying Process in the Age of AI

My sense for now is that I don’t think HO will get anywhere near 50% territory bound online, at least not for a very long time, and a knowledgeable human agent enabled with technology will remain the easiest way to buy HO insurance as opposed to outsourcing judgment to an LLM.

In fact, one possibility is that AI will enhance the viability of independent agencies. How could this happen?

One dimension is data. The data that is fed to an LLM is of paramount importance to the quality of inference and output. The highest quality data is that of real consumers, claims and losses across a variety of carriers. Who has that data? Scaled independent agencies. If scaled independent agencies can apply that data with AI, maybe it makes their service offering better.

If LLMs were actually capable of taking a consumer all the way through the binding process, or right up until the moment of binding, they’d have to be highly integrated into the carrier writing that policy. This takes more technological work than meets the eye; Goosehead’s quote-to-issue (QTI) integrations for three carriers took over a year to implement, and the lack of speed was mostly attributable to the carriers. So if AI technology is going to disintermediate insurance distribution, carriers will need to be in the driver seat.

Another dimension is simply AI-integration into simple policy service requests like adding an insured, adding an auto, tweaking coverage, etc. Instead of humans handling those requests, either via email or on the phone with customers, AI could handle those requests, freeing up human service agents for higher-value tasks and/or reducing the overall need for service labor. This would be a significant cost savings.

That said, nobody knows what is going to happen in personal lines insurance distribution. But taking a look at all of the facts and engrained consumer behavior, along with acknowledging the history of narratives in the early 2000s, leads me to believe that any major structural shift with the way HO insurance is bought is unlikely or would otherwise take decades to unfold.

Recap

- Personal auto and homeowner (HO) policies are non-discretionary purchases

- In terms of total written premium, personal lines is a $530B industry, $170B of which is HO

- In HO, rate/price is driven by exposure growth and has outpaced base inflation. Severe convective storms and wildfires are increasingly responsible for a larger share of insured losses

- Personal lines P&C is fragmented at the carrier level and at the distribution level

- In HO, the independent agency channel has gained significant share at the expense of captive carriers. This has been and will likely continue to be a structural tailwind

- Personal lines P&C, particularly HO, is currently working its way out of a protracted hard market, which should be a tailwind for policies written going forward as rate growth moderates

- A narrative that AI will disrupt and disintermediate insurance agencies and brokers emerged in February 2026; this closely resembles a narrative in the early 2000s as the Internet surfaced as a potential disruptor to distribution. It took nearly three decades for auto insurance to sniff the 50% bound-online mark, and HO is a meaningfully more complex product. Therefore, I do not believe the disruption narrative is plausible in the near and intermediate term