Part 3: Insights from Talking to 15+ GSHD Agency Owners

The core growth engine of a personal lines insurance business, especially an insurance distribution business, is its producers. The most important KPI for this business is growth in policies in force (PIF), and it’s the top priority of individual producers to grow PIF. Any agency business designed around optimizing this metric should naturally do well.

There are about 2,100 franchise producers across about 1,000 franchise agencies in the Goosehead system. These producers represent about 80% of producers system-wide (including corporate producers).

Since late 2025, I’ve talked to over 15 Goosehead agency owners. These owners ranged from one year of tenure to 3+ years of tenure, 24 years of age to 50+ and 12 states (CO, NV, OR, NV, MT, AZ, TX, WI, OH, MI, SC, ID).

I’ve organized my takeaways into several insights below.

My overall assessment of the Goosehead agency business is that it’s a great business, yet there is an extreme minority of agency owners who are actually running their agencies like a business. The most productive, young agencies tend to be owned by producers in their early 20s, with no business experience. They are simply killers when it comes to selling new policies, and it rubs off on their entire team. This is also a sign, in my view, that the Goosehead agency model is innately geared for growth.

I have no issue with a business that works so well that it doesn’t require astute managers to produce a lot of cash.

1. The Goosehead agency model works very well for PIF growth, but the playbook has to be followed

What’s different about Goosehead agencies compared to almost every other personal lines independent agency?

The sales function and the service function are separated so that each can enjoy its comparative advantage. The workflow and skill set of selling new insurance policies is much different than the workflow and skill set of servicing and maintaining existing policies. They are also each time consuming. By centralizing the service function within corporate, franchise producers are freed up to focus on selling new policies.

Selling new business is a volume game, so the more time that can be applied to new business, the faster the growth of the agency.

The royalty structure is also set up to incentivize franchise producers to focus on selling new policies. Goosehead takes a 20% royalty on new business commissions and 50% on renewal commissions. There are a couple of incentives that fall out of this. The first is obvious, which is that in any given year, a producer makes more money on a new policy sold than an existing policy retained. It is more within control to sell a new policy, so that’s where the focus should be.

The second incentive is less obvious, which is that when the book becomes larger multiple years after starting, there is still a strong incentive to continue growing the book instead of plateauing. With a service function that is not centralized and within the responsibility of the producer, like it is at a small independent agency or a captive agency, larger books mean more time spent on service. With ample residual income, the producer has a declining incentive and declining time and energy to spend on selling new business. So there is a lasting incentive for new business generation, which translates to agency growth.

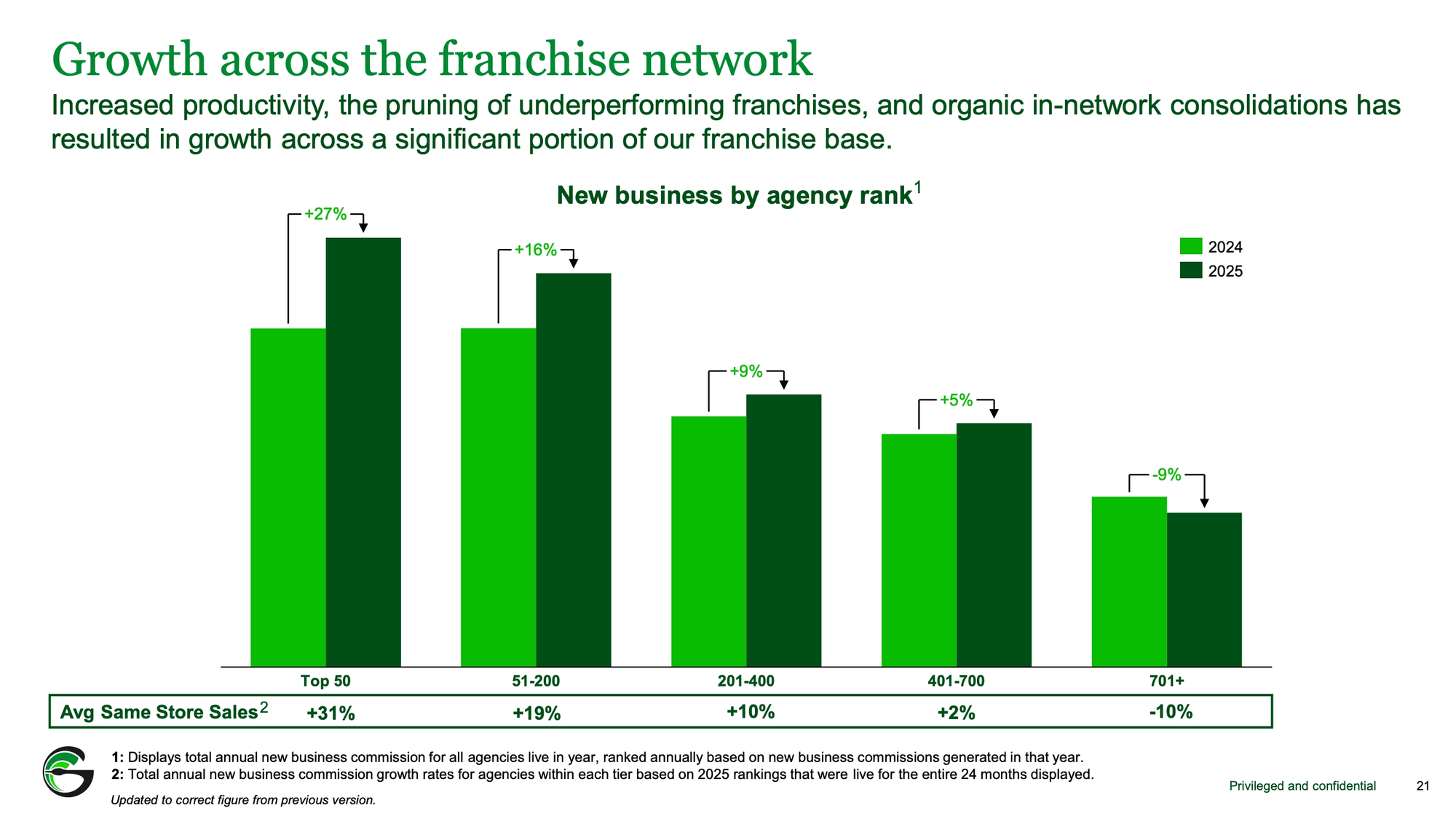

As agencies get larger, they tend to do better with growth. This is mostly attributable to their commitment and ability to hire new producers. Management has cited that a new producer hired into an existing franchise is 1.7x as productive as the average new franchise. Recently, the company also disclosed same-store sales metrics based on agency size, which also suggests that larger agencies are more productive than smaller agencies.

The model should show an ability to produce some astounding sales numbers, and it does. The overall record for one month’s sales was achieved in March 2026 by an agency owner in his early 20s, selling 240 new policies in 22 business days. Over 10 new bound policies per day is a huge number. At a captive agency, the bind rate might be 15% or less, which would imply that a captive agent would need to quote over 60 policies per day to bind the same 10. In an 8-hour workday, that would mean one quote every 8 minutes with no breaks. I think that would be impossible.

Outlier aside, the industry-leading productivity of the model also came through anecdotally in my conversations. Several middle-aged owners who joined Goosehead after having been at captive carriers for a number of years told me that they grew their Goosehead book from $0 to the size of their old captive book in just a few years. ”Four years in, I’m making way more money with Goosehead than AAA” and “I was at AmFam for 16 years, my book is bigger now at Goosehead in less than 5 years.” The overall average at Goosehead stands up well to the industry.

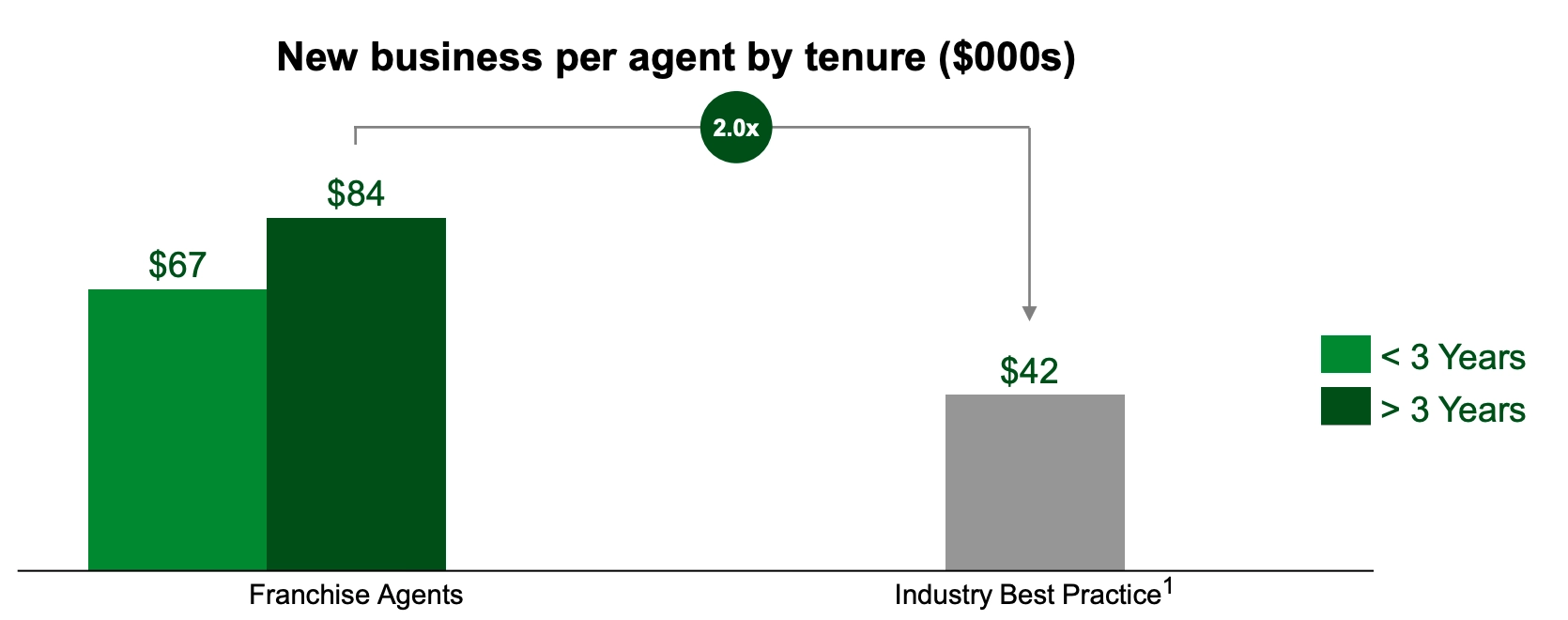

Another observation that emerged from my conversations was that younger agency owners do very well with the Goosehead model. These are typically owners in their early 20s, and have either done nothing before Goosehead or have had one prior work experience. The corporate agency also focuses heavily on this age group for new producer hires. This tells me that the model is easy to learn, it has tech that is intuitively grasped by younger people and that there is a high ceiling for those capable selling at high volumes with speed. The company says that corporate producers who transition to the franchise channel are 13x more productive (new business) than external recruits.

An additional proof point that the model works well is the bind rate. The bind rate is the number of policies sold divided by the number of policies quoted. At Goosehead, the bind rate is in the 40-50% range based on what I heard from owners. This is double or more than double captives, which are at sub-10% to 20%. Drivers of a higher bind rate at Goosehead are 1) choice of several carriers and coverages, so a customer knows all of the options when talking to a Goosehead agent and has no further research to do, and 2) the Goosehead model is built for speed, which is helpful in avoiding customer deliberation and helpful in a home-buying process where speed is valuable.

The ability of the Goosehead model to support a very high ceiling on new business generation cannot be understated. While the renewal royalty appears high on the surface at 50%, the tradeoff is the vast majority of producers’ time can be spent generating new business — not servicing the existing book, managing a service staff and managing IT infrastructure. Additionally, the bulk of that 50% royalty is effectively payment for the service staff and the IT infrastructure they would otherwise be paying if they were independently owned. Said another way, the tradeoff is the ability to have significantly higher volume and revenue that outweighs any margin savings without the 50% royalty on renewal revenue. Without the Goosehead model, the same producer would do lower volume elsewhere.

The caveat to the model is that if the playbook is not followed, growth is much harder. The playbook for a GSHD producer is twofold: 1) focus almost all of your time on new business, and 2) use the established go-to-market strategy, which is building referral relationships with mortgage/loan and real estate professionals.

The biggest mistake in not following the playbook that I gathered was that agents were spending too much time on service. These agents tended to be older in age and they previously spent many years at captive agencies. This took their time away from generating new business.

The most common solution to fending off time spent on service is training and guiding clients how to use the service function at Goosehead. In other words, it is setting expectations upfront and explaining really well that when they have service related questions or requests, there’s a separate team to contact. That’s not to say that the originating agent cannot be friendly and helpful to their clients and maintaining a relationship, but the bulk of the work and service time should be done by the service team.

2. A directive to agencies to focus on growth has been a significant sentiment shift in the last year

The majority of agency owners I talked to discussed an almost forceful directive from corporate for franchise agencies to focus on growing their books. In other words, they want each agency to reach the size where it makes sense to hire more producers, or if they are at that size, to hire more producers. If agencies don’t grow or are not focused on growth, the message was basically that they’ll be managed out of the system.

“The tone with Goosehead has really shifted, they want people to build mega agencies, ‘think big.’”

“Sentiment has changed tremendously over the past 6 months. They are prioritizing the bigger franchisees.”

In fact, this has been going on for a few years, management has talked about it, and it has played out in the total operating franchises number.

It may seem obvious to focus on growth at the franchise agency level, but it’s an indication of the point in the system’s life cycle of growth. The franchise channel started in 2012, and since then, most of the growth has come from opening new franchises. Throughout the first wave, which was a decade or so, about three-fourths of new franchises were started by agents who came over from the captive carriers. It was a land grab. COVID also provided an accelerant to new franchise openings because opening an agency with little capital was an attractive proposition for entrepreneurial types with seemingly less stable full-time positions. Franchises reached a peak of 1,400 in Q2 2022 and is now back down to 1,000.

Over the last couple of years, and still today, the focus is on growing each agency versus growing the number of agencies.

On that front, corporate launched ASP (Agency Staffing Program), which is an in-house recruiting team that recruits producers for placement in franchise agencies. Agencies pay a small fee to cover the cost, and importantly, they receive the valuable institutional know-how for hiring well. Hiring new producers with high success rates is a pain-point in the industry broadly, with Reagan reporting hiring success rates in the 30-50% range.

Of the owners who talked about ASP (either they brought it up or I asked), there was unanimous support and positive reviews for the program. Many are using it for most of their hires, and at a high success rate. They find it valuable because it has been working, and they as owners do not need to sink a lot of time into hiring their producers.

3. The service function has mixed reviews.

The most common point of dissatisfaction among owners was the reliability and quality of the service function.

Of those expressing dissatisfaction, it was because they thought that they were having to spend more time than they were told they’d have to spend servicing their clients. As mentioned previously, Goosehead’s model is set up so that service is centralized and not done by the selling agents, and that is how they pitch the model.

Wait times (i.e., hold time on the phone) and simple errors were among the specific issues discussed.

Among those who experienced issues, some mentioned that the service function has been improving in the last year or so, and especially over a longer period of time. There is apparently newer leadership trying to improve the system and technology around service. There was also apparently a staffing shortage that management acknowledged and subsequently addressed.

A former captive agency owner told me that “even though service is flawed, it still takes a lot off my plate, and without them I’d be more bogged down.”

Other owners did not have much of an issue with service. These tended to be younger owners, owners of agencies that were growing quickly or owners of agencies that were larger. When I asked them whether they’d had issues with service, a common response was that it’s important to know how to use the service team and function well and to coach clients on how to use it well. Providing feedback to the service team on specific issues has also been constructive.

It’s also important to note the the last few years have been a hard market, where clients are seeing rates rise significantly. This is an inherent and significant barrier to client satisfaction, so any issues with service may be magnified.

Overall, my assessment is that the performance and staffing level of service is an area to monitor, but it is not cause for concern. An indicator to watch is client retention and the NPS score as the market softens (i.e., rates come down). If these do not rise when rates fall, I might start to question the performance of the service function.

4. The tech platform has positive reviews.

Many agency owners cited the tech platform as one of the major positives of Goosehead relative to other models. No owner I talked to was dissatisfied with the tech.

This is noteworthy validation, because Goosehead has pitched itself essentially as a tech company that happens to sell insurance. I think that takes it a step too far, but the tech platform that agents use is proprietary, and I do think it enables the volume and speed that sets Goosehead apart in new business production.

The tech platform enables volume and speed because all of the tools agents need are incorporated into one system — data on referral partners, comparative rater, quoting, CRM. Agents don’t have to learn and have workflows across multiple tools and are able to do everything remotely from a laptop.

I intend to understand what exactly differentiates the tech in more detail going forward, and I’ve made outreach to tech-focused professionals who have been exposed to the Goosehead platform.

5. M&A is active within the franchise system.

One of the ways that underperforming books or books from owners who want to exit the system are managed out is selling to existing franchises. Several of the owners I talked to were either 1) open to eventually selling their book or knew of other small franchises looking to sell their books or 2) have purchased other books within Goosehead (and externally in one case).

A healthy M&A market is positive for the long-term growth of the system. For owners who have become less interested in growing their agency, selling their book means they can exit without simply handing over their book to corporate for nothing. This provides an incentive to move their book to ‘growthier’ hands instead of hanging on to their plateaued book.

It’s also a positive signal that there are willing buyers with the financial wherewithal to buy books and smaller agencies. In my conversations, it was also apparent that debt financing for these purchases is attainable. I spoke with a loan officer at Live Oak Bank who works on insurance agencies, and he told me that 90% of his Goosehead lending is for M&A.

As the largest agencies continue their growth, M&A will continue to be a lever they can pull to sop up the underperforming and smaller agencies to expand geographically. This is a net positive for the franchise channel, because larger agencies tend to have better per-producer productivity and greater longevity relative to smaller ones.

Recap

- The Goosehead model is designed for PIF growth, and that is what it delivers. The ceiling for new business productivity is high and industry-leading

- There has been a sentiment shift in the last year from corporate to the franchise network to grow their agencies, primarily through hiring new producers

- The separated, centralized service function at Goosehead makes sense for the model but has delivered inconsistent reliability. There’s been a recent effort by corporate to improve the service function

- Agency owners speak highly of the tech platform. More work to be done to understand in more detail the differentiating features and technical factors of the platform

- M&A is prevalent within the Goosehead system and is a healthy mechanism of the system long-term