QXO: What's the price?

Getting the current price of a public company should be something that anyone with an internet connection and no financial knowledge can do today. A 16-year old with no knowledge of business or markets could probably figure out how to ask ChatGPT for such information, or know that it has to be somewhere on the Robinhood app, probably a few swipes after the NFL prediction market and crypto pages.

But getting an accurate current equity value of a company is not always that easy.

If you go to Yahoo! Finance and look up the current market cap of QXO, it tells you it is approximately $16.0 billion at the current market price per share of $23.81 as of closing on January 16th. Turns out, a $16B market cap for QXO is simply wrong. Quite significantly wrong, actually. The accurate market cap of QXO is actually about $28 billion, or 75% higher than Yahoo! Finance says. This is a problem! Particularly since stocks are more-easily-than-ever available for any retail investor to buy.

Obviously, understanding the true price of something you are going to buy couldn’t be more fundamental to any purchase decision. This is basic stuff.

But, in my 10+ years of investment banking, I’ve seen even finance professionals can fall prey to the inaccurate shortcuts, including looking up the market cap of a company on Yahoo! Finance and believing what it tells you.

Understanding QXO's equity value requires work

For emerging students of finance, a quick word. The issue with data services like Yahoo! Finance (and even the institutional standard Bloomberg, sometimes) is they show you market cap or equity value based only on basic shares outstanding. In other words, they exclude certain shares — shares from very recently completed equity offerings, shares from convertible preferred stock or convertible notes that are in-the-money and shares from RSUs and stock options. Another common trip-up among practitioners is the Up-C structure, where part of the equity is represented economically by private LLC units (which have common equity share classes that track these LLC units for voting purposes). All of these shares represent real ownership in the equity, and economically, they must count.

So what are QXO’s dilutive securities? There are many:

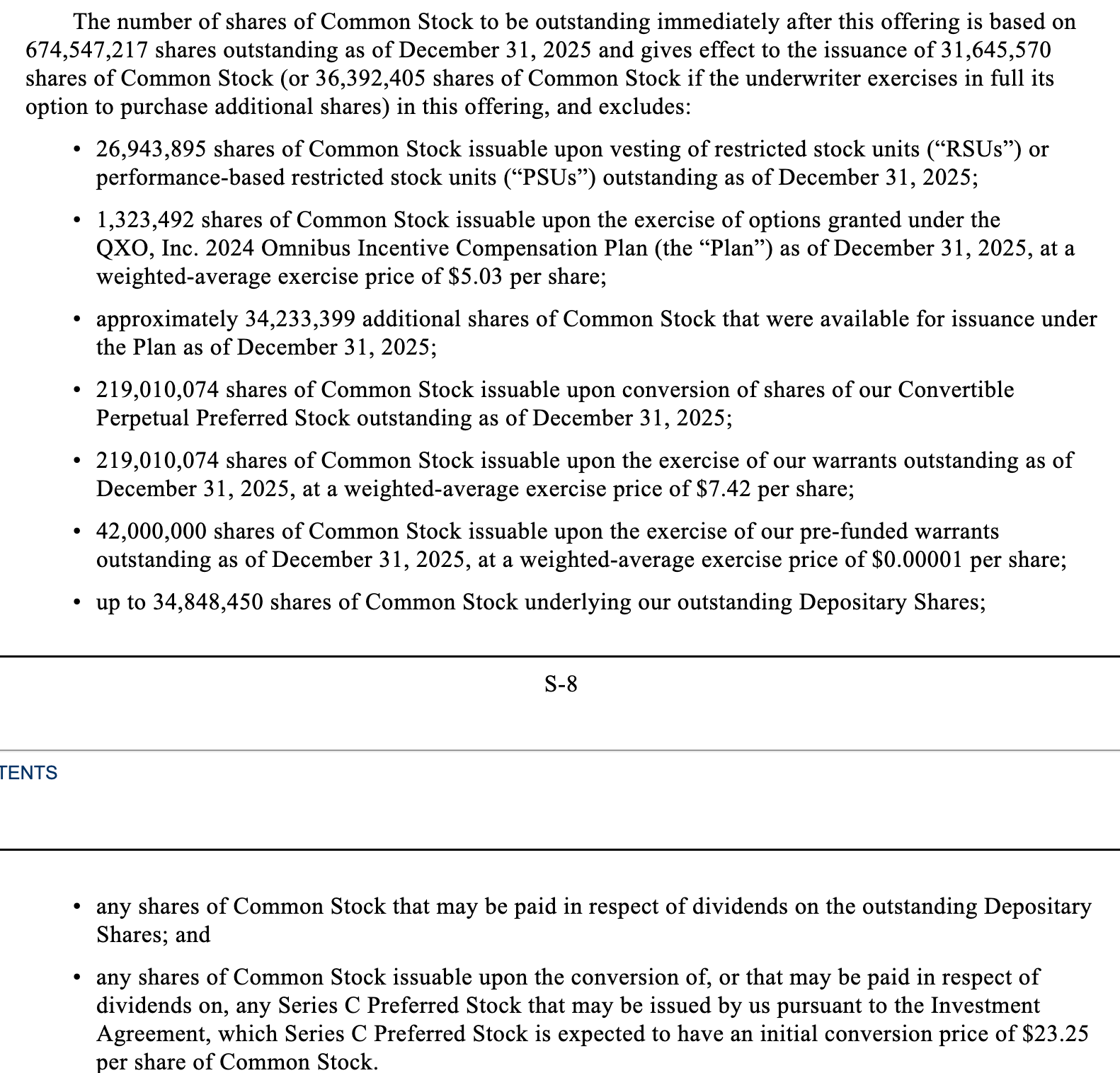

- Shares recently issued from a common stock offering (i.e., shares not yet in the share count reported on the face of the 10-Q)

- RSUs and PRSUs and stock options

- One set of priced warrants, inclusive of three tranches at different exercise prices

- One set of pre-funded (i.e., penny) warrants

- Convertible preferred stock (the original investment from Jacobs)

- Depositary shares representing an interest in Series B mandatory convertible preferred stock (the Depositary Shares are publicly traded at a different price, implying a current market value for this Series B preferred implies a premium to the common, and should, because of priority and dividends)

Another note to emerging students of finance: you discern the list above by a) most often, a careful reading the Equity footnote in the financial statements, b) if the company in question has recently issued equity, the summary in the most recent prospectus will give you a nice list, and/or c) if the capital structure is complex, the company may show you the math in an investor presentation. In the case of QXO, b and c are available in addition to the always-available a.

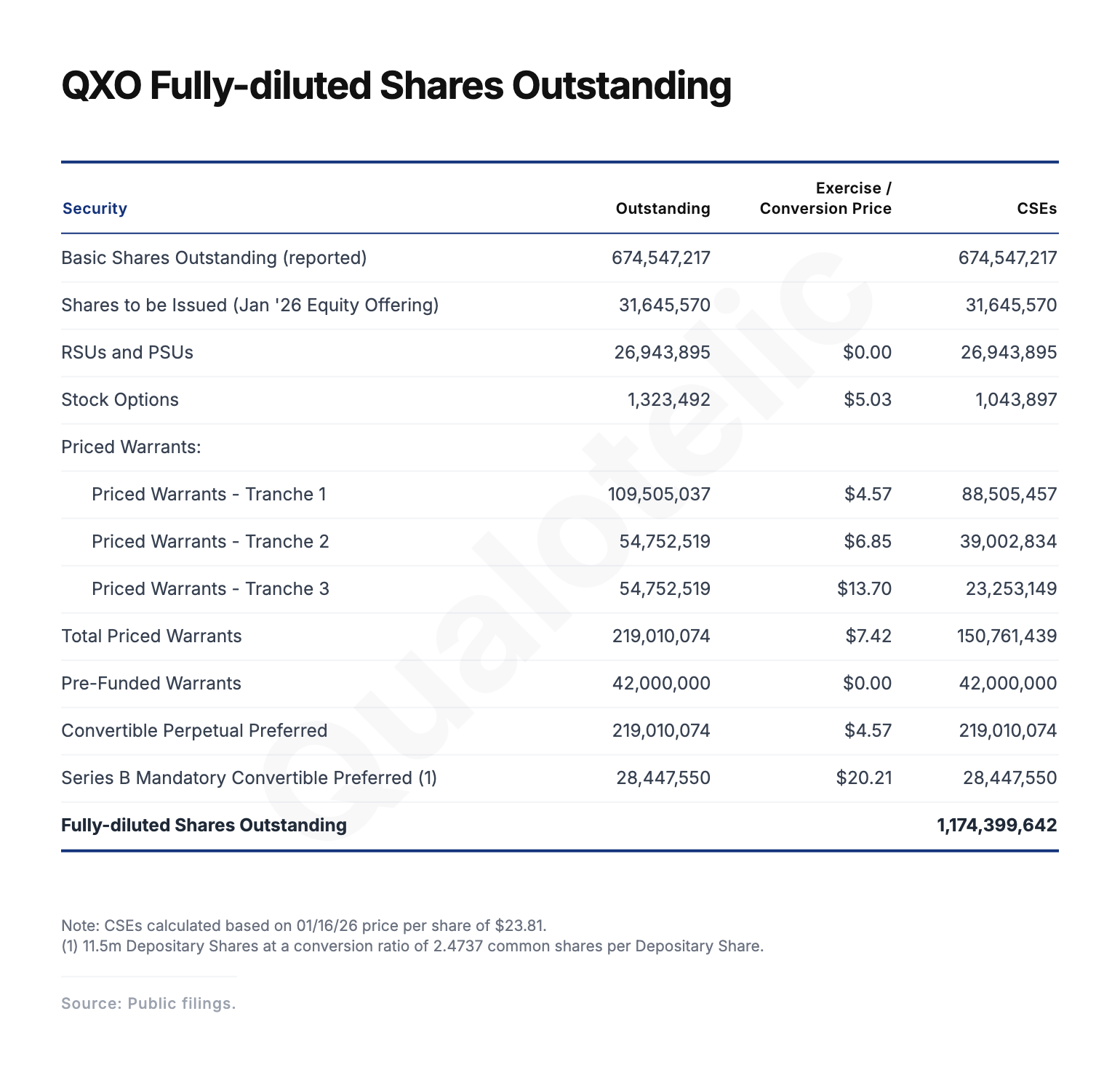

Putting this all together, here is the calculation of QXO’s current fully-diluted share count:

Note that we have not included any dilutive securities from the recent Series C convertible preferred stock issuance because these shares are not yet issued and the cash is not yet received; this will happen in the future concurrent with the closing of an qualifying acquisition. This is basically committed equity financing for a potential acquisition, and while it is more likely than not that QXO will complete these potential acquisitions, today’s share price does not reflect the financing or economics of such targets. Generally, we would not count these shares until the acquisition is closed.

So, we have 1,174.4 million shares at $23.81, equating to a market cap of $28 billion.

What is the common shareholder getting for the price of $28 billion?

Taking a step back…what is the business of QXO?

From the January 16, 2026 prospectus (bold added):

QXO was created in 2024 to build a tech-forward leader in the approximately $800 billion Building Products Distribution sector. QXO was founded by Brad Jacobs, a serial entrepreneur with a strong track record of value creation. QXO is targeting $50 billion in annual revenues within the next decade through accretive acquisitions and organic growth.

Over the course of his career prior to QXO, Mr. Jacobs started five highly successful companies that he and his teams built into billion dollar or multi-billion dollar publicly-traded enterprises. These include XPO, Inc. (NYSE:XPO), GXO Logistics, Inc. (NYSE:GXO), RXO, Inc. (NYSE:RXO), United Rentals (NYSE:URI) and United Waste Systems. In 2024, QXO recruited a number of experienced executives to execute on a business plan involving the acquisition, transformation and integration of companies in the Building Products Distribution sector in North America and Western Europe. Our team members have differentiated experience executing on acquisitions, integrating acquired businesses and driving transformation, at scale, to maximize profits.

Since Jacobs took over in early 2024, QXO made its first acquisition, the $10.6B purchase of leading North American roofing distributor Beacon for 11.4x EBITDA in April 2025, and raised approximately $16.6 billion of cash (including the recent $3B preferred stock commitment).

If you’re purchasing the equity today, you are effectively buying:

- Equity value in the legacy Beacon business, which we can value as roughly $7.5B (purchase enterprise value less current debt of $3.1B)

- Excess cash on the balance sheet, which we can say for simplicity is the current cash balance after the most recent equity raise, or $3.1B

- Which, after deducting these from current market equity value, leaves $17.4B implied value of the future upside of QXO

In other words, you’re paying $17B today for the value creation story or option value that is QXO and its management team’s track record. A satisfactory annual return would need to justify this price on its way to growing to something much larger over a number of years. What kind of annual return is the market currently pricing in?

Estimating the current return opportunity

We can get a rough estimate of potential returns on the equity by working down from QXO’s target of $50B of annual revenue within the next decade. Of course, doing so requires a number of assumptions. Despite limitations that come with making a handful of assumptions, we can attempt to get a directional sense of the return profile.

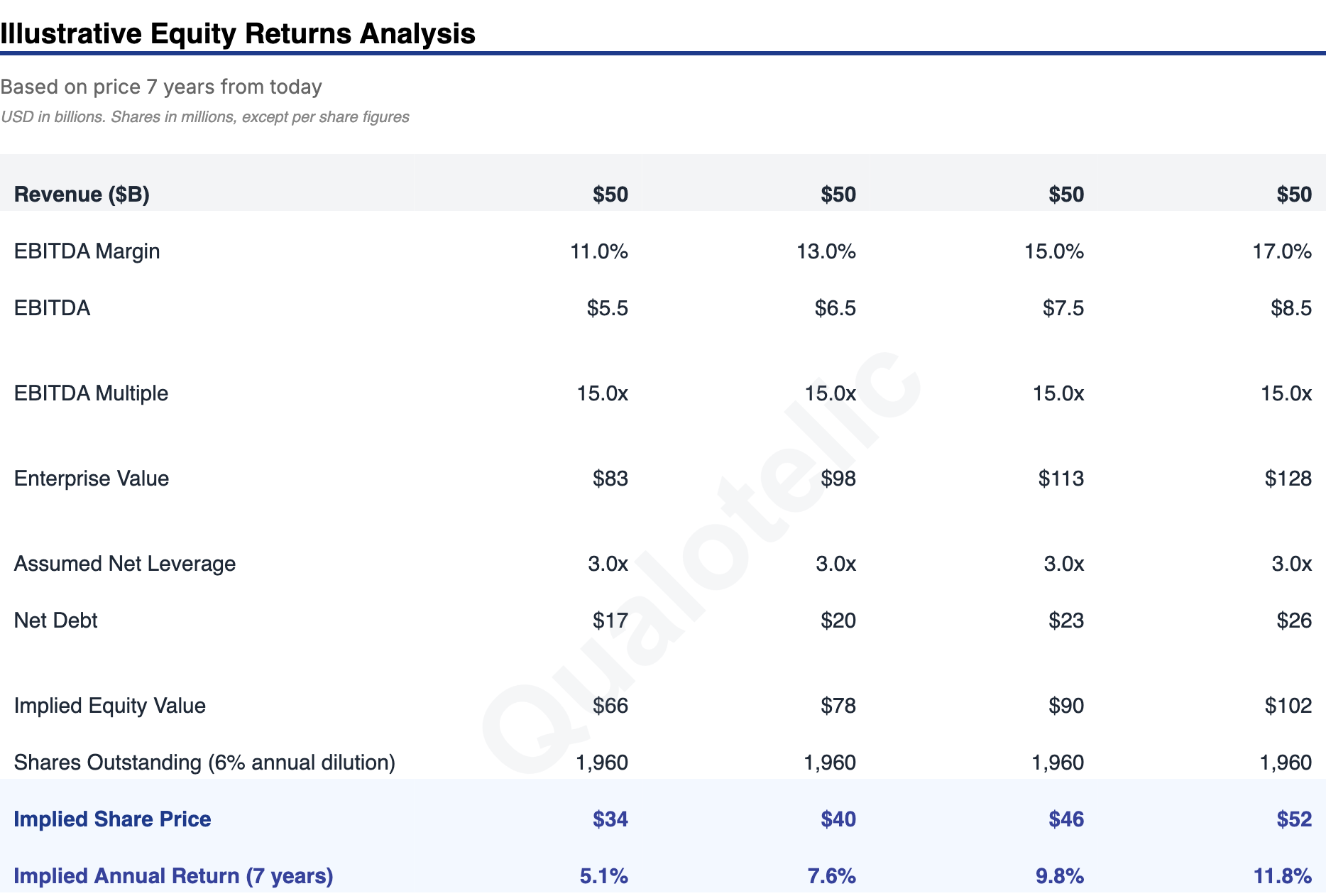

For purposes of an initial analysis, let’s make the following assumptions:

- $50B revenue achieved in 7 years. Management has said “within the next decade.” $50B in 7 years from call it $9.5B today is 27% annual growth. The assumption is that this is going to include significant M&A

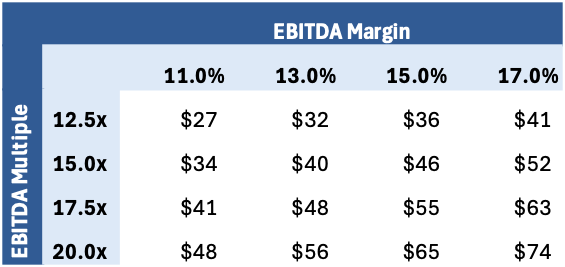

- A range of EBITDA margins of 11% to 17%. For a distributor in this industry, this range I’d estimate to be pretty rich. Scaled peer BLDR sports an 11% margin, and Beacon had a 9% margin in 2024. Scaling a technology-native distribution business should result in operating leverage, but this would require great execution

- An EBITDA (1) multiple of 15x. SITE and POOL trade around this area, BLDR trades HSD/LDD and Beacon was acquired for over 11x. With above-average growth and capital allocation, QXO could earn a multiple premium. 15x EBITDA does not feel out-of-hand, and maybe it achieves yet a higher premium, but 15x for a base case feels reasonable

- Net leverage of 3x at our future valuation date in 7 years. Future EBITDA will have been a result of acquired EBITDA and EBITDA achieved through organic growth of a) Beacon and b) future acquired business. The acquired EBITDA will be financed with a combination of debt, newly issued equity and free cash flow

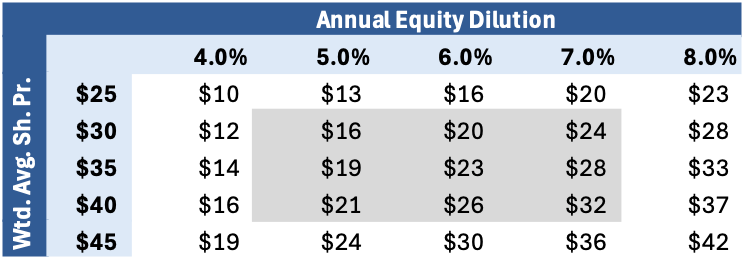

- Annual equity dilution of 6%. There will be equity dilution as a result of newly issued shares to fund acquisitions and for employee compensation (a real cost to the non-employee common shareholder!). We will sensitize this assumption to see what higher levels look like

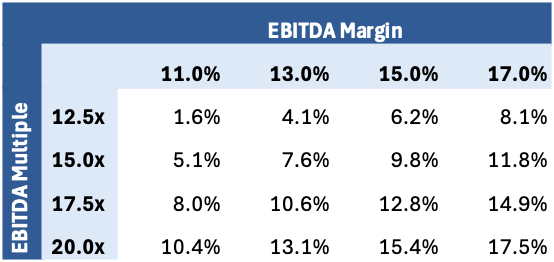

These assumptions result in a future price per share of $34 to $52 (Year 7), implying an annual return from today’s price of 5% to 12%:

The annual equity dilution assumption is important, as each point of dilution costs about one point of annual return in our analysis relative to assuming no equity dilution. This makes sense — for every 10% enlargement of a pie we own, assuming we do not purchase more equity, we’re left with 91%, or 9% less, of the whole. Hopefully, the whole is getting more valuable at a rate higher than the dilution (and cost of capital).

In theory, QXO will be issuing shares at a per-share value that is at most equal to the per-share intrinsic value of the businesses being acquired, so that the equity holder is receiving in value at least what has been paid in issuing more equity. When a business buys another business with equity, it is the same thing as selling a part of itself, at its current price, to buy a business at its acquisition price. Implicit in the decision to make this purchase is understanding what QXO itself is worth…a very difficult question! Even better than receiving in value exactly what was paid is if QXO pays a price less than the target’s intrinsic value — either by being a shrewd buyer (less common) or by executing an integration and operational plan that produces synergies and operating leverage (very commonly talked about and promised, less commonly achieved). In these cases, acquisitions will be value-generating. This is at least half of QXO management’s thesis, and the track record for acquisition and integration and shareholder value creation is very good. The purpose of this analysis is to figure out how much you might be paying for that.

Back to the analysis, how do we gauge whether the 6% assumption is a reasonable one? We can make some assumptions about how much of the EBITDA by Year 7 has been acquired, the price paid for that EBITDA and how much of that is debt and equity financed. The caveat here is that this is directional analysis.

This shows that the acquired EBITDA requires $16B to $32B of financing from either new equity or cash flow. In the center shaded values of the sensitivity below, we see the range of 5% to 7% annual equity dilution at a weighted-average stock price during that time of $30 to $40 per share impl. These assumptions are debatable, but we’re working with something directional.

Required Financing from New Equity:

What do future share prices and returns look like if the EBITDA multiple isn’t 15x, and is either lower or higher? To get into 15%+ return territory, you’d have to believe in a 17% EBITDA margin at a 15x multiple or a 20x multiple at a 15% EBITDA margin.

Future Share Price:

Future Returns:

Worthy of more work?

Based on this analysis alone, which may be used as a starting place to decide to do (a lot) more work, the market’s current price does not seem to offer an obviously compelling opportunity. In other words, I think the market is pricing QXO at a barely reasonable to a moderately aggressive price. There clearly isn’t a margin of safety.

This is not surprising given Jacobs’ prior track record. As Warren Buffett said of Tom Murphy, “If Murph should elect to run another business, don’t bother to study its value—just buy the stock. And don’t later be as dumb as I was two years ago when I sold one-third of our holdings in Cap Cities for $635 million (versus the $1.27 billion those shares would bring in the Disney merger).” If you know Brad Jacobs well, and you believe in his ability to create value, maybe QXO is today’s version of the Murphy-led Cap Cities. There are many worse bets to make out there in today’s market.

Additionally, it’s not difficult to see that the building products industry could be ripe for value creation in the coming decade. Consensus suggests that there is a housing shortage in the U.S. today (QXO estimates a shortage of 4 million housing units) which based on the level of annual new housing starts and new household formations, could take up to a decade to alleviate. Housing affordability is in a trough (high interest rates, high home values, interest rate lock-in effect), and with homebuilding being perceived traditionally as a cyclical industry (that might be changing), it is a bit out of favor at the moment. When that turns, value-added distributors like QXO should see increased demand. The housing stock is also aging at about 40 years, which would support increasing demand for renovations.

So some of the bigger questions really become:

- What if there really isn’t as much pent up demand for housing as is currently perceived? What if more and more people start preferring to live in multi-family units (e.g., apartments, condos) instead of homes?

- How achievable is the $50B revenue target for QXO in the next decade? How much market share does this assume they must take?

- How competitive will the M&A market be for compelling assets? QXO already lost a bid for GMS to Home Depot’s distribution subsidiary. How will this affect future prices paid? If QXO struggles to win assets, does this add to the $50B revenue timeline?

All of that said, I will be watching QXO, primarily for learnings from its method of execution, both on M&A and operationally. I’m also curious about Jacobs’ capital allocation talent, which I think is more likely than not that he has both the talent and the focus on its importance for shareholder value creation (I note the story about him deciding to do a $1.5B buyback at XPO on the heels of a short report that sunk the stock).

- I’m taking “EBITDA” for granted here. One must earn the right to use multiples…everything is a discounted cash flow. But, since we are comparing EBITDA multiples to peers here, and we’re doing a preliminary analysis, we’re simplifying with EBITDA as reported. Things like stock-based compensation will commonly be added back for EBITDA these days…and for valuation purposes, that’s a problem.